人工智能技术的发展和应用前景

版权申诉

191 浏览量

更新于2024-07-03

收藏 3.27MB PDF 举报

人工智能概述

人工智能(Artificial Intelligence)是信息时代的顶级技术。随着机器学习和深度学习的进步,结合更加强大的计算能力和不断扩展的数据池,人工智能正在逐步走近公司跨行业的应用范围内。

人工智能作为服务的发展拥有打开新市场和打破云计算领域格局的潜力。我们认为,能够充分利用人工智能的能力将成为公司未来的竞争优势关键属性,并将带来生产率的复苏。

以下是人工智能概述的相关知识点:

一、人工智能定义

人工智能是指通过机器和计算机系统来模拟人类智能,实现自动化、智能化和自适应的技术。人工智能包括机器学习、深度学习、自然语言处理、计算机视觉等领域。

二、人工智能的应用场景

人工智能的应用场景非常广泛,包括但不限于:

* 客户服务:人工智能可以应用于客户服务领域,例如智能客服、自动化客服等。

* 数据分析:人工智能可以应用于数据分析领域,例如数据挖掘、预测分析等。

* 图像识别:人工智能可以应用于图像识别领域,例如人脸识别、物体识别等。

* 自动化生产:人工智能可以应用于自动化生产领域,例如智能制造、自动化装配等。

三、人工智能的技术架构

人工智能的技术架构主要包括:

* 数据层:数据层是人工智能的基础,负责数据的采集、存储和管理。

* 算法层:算法层是人工智能的核心,负责算法的设计和实现。

* 应用层:应用层是人工智能的最终应用,负责将算法应用于实际场景中。

四、人工智能的挑战和机遇

人工智能面临着许多挑战,例如数据隐私、算法公平性、工作岗位替代等。但是,同时人工智能也提供了许多机遇,例如提高生产率、改善生活质量等。

五、人工智能的发展趋势

人工智能的发展趋势包括:

* 云计算人工智能:云计算人工智能是指将人工智能技术应用于云计算领域,提供更加智能和自动化的云计算服务。

* 边缘人工智能:边缘人工智能是指将人工智能技术应用于边缘计算领域,提供更加快速和智能的边缘计算服务。

* Explainable AI:Explainable AI是指能够解释人工智能决策过程的技术,提高人工智能的透明度和可靠性。

人工智能是信息时代的顶级技术,具有广泛的应用场景和技术架构。人工智能的发展趋势包括云计算人工智能、边缘人工智能和Explainable AI等。

November 14, 2016 Profiles in Innovation

Goldman Sachs Global Investment Research 16

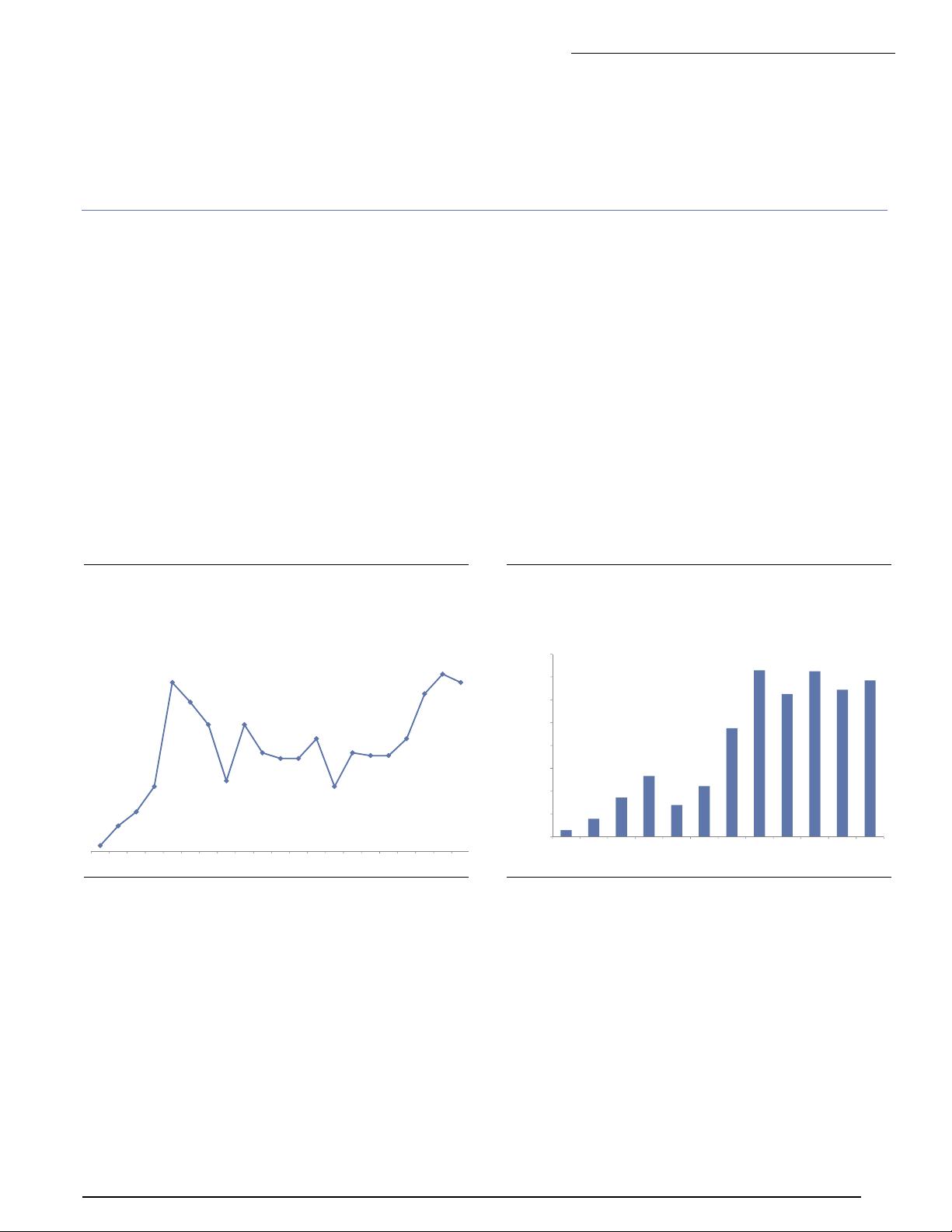

operations processes contributed to creating a threefold spike in growth (output per labor

hour) during the 1990s, with IT-producing sectors responsible for at most 49% of the

average annual increase in annual productivity growth from the pre-boom period to the

period between 1995 and 2004 (Exhibit 10).

Exhibit 10: Late 90s: IT-producing sectors contribute nearly half of productivity growth

But lose value and share in growth post-tech boom

Source: Federal Reserve Board, Goldman Sachs Global Investment Research

Post-millennium stagnation. During the past decade, capital deepening growth related to

IT applications (computer hardware, software, and telecom) has stagnated. IT capital,

relative to broader market capital, has contributed less to overall growth in this component

than average contributions during and even before the tech boom. Aggregate labor hours

have been increasing, but the contribution of capital intensity to productivity has drastically

underperformed versus the 1990s. The introduction of increasingly sophisticated,

consumable machine learning and AI may be a catalyst in bringing capital intensity back to

the forefront, in our view, significantly increasing the productivity of labor similar to the

cycle we saw in the 1990’s.

We’re more optimistic on the MFP side of the equation. GS economists have highlighted

(Productivity Paradox v2.0 Revisited, 9/2/2016) that upward biases on ICT prices and a

growth in inputs towards unmonetized outputs (free online content, back-end processes,

etc.) add to the understatement of real GDP and productivity growth. Evolution of internet

giants like Facebook and Google highlight the idea that complex input labor and capital

aren’t necessarily converted into traditional consumer product monetization captured in

standard productivity metrics.

AI/ML induced productivity could impact investment

We believe that one of the potential impacts of increasing productivity from AI/ML could be

a shift in the way companies allocate capital. Since mid-2011, the growth in dividends and

share repurchases has significantly exceeded capex growth, as reluctance among

management teams to investment in capital projects remains post-recession.

0.77

1.5

0.64

0.79

1.56

0.92

0

1

2

3

4

1974-1995 1995-2004 2004-2012

IT Contribution Other nonfarm business

% growth

1.56% total average

growth virtually equal

to 1995-2004 average

IT contribution

via:资料来源网络,起点学院学员收集

起点学院www.qidianla.com,互联网黄埔军校,打造最专业最系统的产品、运营、交互课程。

剩余98页未读,继续阅读

点击了解资源详情

点击了解资源详情

点击了解资源详情

2019-06-09 上传

2018-10-24 上传

2023-02-27 上传

2021-04-23 上传

2019-07-20 上传

2022-07-01 上传

黄啊码

- 粉丝: 1w+

- 资源: 2313

我的内容管理

展开

我的内容管理

展开