5G相控阵天线技术革新与市场前景

需积分: 10 160 浏览量

更新于2024-07-17

收藏 4.53MB PDF 举报

"《2019年MACOM关于5G相控阵天线的创新技术与应用》电子书深入探讨了5G无线接入网络(RAN)中相控阵天线系统的关键创新和发展。该书由Gary Lerude撰写,作为Microwave Journal的技术编辑,它为读者提供了对5G通信技术路线图的全面理解,特别是与波束形成的空间复用相关的技术。

首先,作者概述了相控阵天线的发展历程和在5G中的关键作用,这些天线通过精确控制信号的相位,实现了更高的频谱效率和方向性,对于5G的高数据速率和大规模连接需求至关重要。书中特别强调了空间复用技术,即多用户多输入多输出(MU-MIMO),它在5G中如何通过在同一时间、同一频带内支持多个用户,显著提高了网络容量。

Doug Carlson,MACOM公司的代表,详细阐述了5G相控阵天线的开发进展,特别是在6 GHz以下和毫米波频段的应用,这两个频段对于5G的部署至关重要。他讨论了如何突破成本障碍,使得这种先进技术更加经济可行,这对于大规模部署5G基础设施是至关重要的。

MathWorks的Honglei Chen和Rick Gentile合作,介绍了软件和硬件相结合的近场变换技术在5G空口测试中的应用。这种技术帮助优化天线性能,确保在实际环境中的通信质量,尤其是在毫米波频段,由于其较高的频率和更短的波长,对天线设计和测试提出了更高要求。

Walter Honcharenko,同样来自MACOM,针对5G的基站设计,探讨了如何在满足5G对尺寸和重量限制的同时,实现毫米波子系统的集成,这是实现移动性和高效能的重要一步。

此外,书中还提到了国防市场的强劲前景,对射频技术(RFT)产业持续增长的影响,特别是由Asif Anwar代表的Strategy Analytics的观点。5G相控阵天线不仅限于民用,也对军事通信产生了深远影响。

《Innovations in Phased Array Antennas for 5G》是一本详尽的指南,涵盖了从技术原理到实际应用的各个环节,为理解5G时代的无线通信变革提供了丰富的洞见。无论是制造商、工程师,还是对5G技术感兴趣的读者,这本书都是深入了解5G相控阵天线创新及其在无线网络中所扮演核心角色的重要参考资料。"

6

Strategy Analytics also predicts:

• North America will continue to represent the largest

regional end market, but the fastest growth will come

from demand in the Asia-Pacic region (see Figure 3).

• Airborne radar will represent the largest market, both

in dollars and total shipments.

• Early warning, surveillance and re control radars will

account for around 76 percent of the global military

radar market.

• L-, S- and C-Band will represent the largest market,

followed by radars operating at X-Band, which reect

the primary frequencies used by surveillance, early

warning and re control radars.

• The total number of radar shipments is forecast to

grow at a CAAGR of 4.6 percent through 2027 to

reach 1,607 units. Fire control radar and early warn-

ing and surveillance radar shipments will account for

48 percent of 2027 military radar shipments.

• The associated market for semiconductors and other

components will grow from $2 billion in 2017 to reach

$5 billion in 2027.

EW

Operational requirements to establish freedom of ac-

tion in contested and congested environments, as well

as the ability to counter modern agile radar and com-

munications will drive opportunities for the EW market.

There is a renewed push to upgrade conventional EW

capabilities that support anti-access/anti-denial (AA/

AD) strategies. This will be coupled with the ongoing

requirement to combat asymmetric threat scenarios.

Future systems will employ wideband solid-state semi-

conductors to enable articial intelligence (AI)-based

machine learning algorithms to provide cognitive analy-

sis of the threat environment. EW will play an important

role in tackling the increasing complexity that comes

with operating in a spectrally constrained environment.

Companies providing systems and enabling technol-

ogies will need to focus on solutions that employ wide-

band materials, such as GaN, and AESA architectures

to enable machine learning-based cognitive analysis,

planning and countermeasures activity that can either

augment or circumvent the traditional threat library.

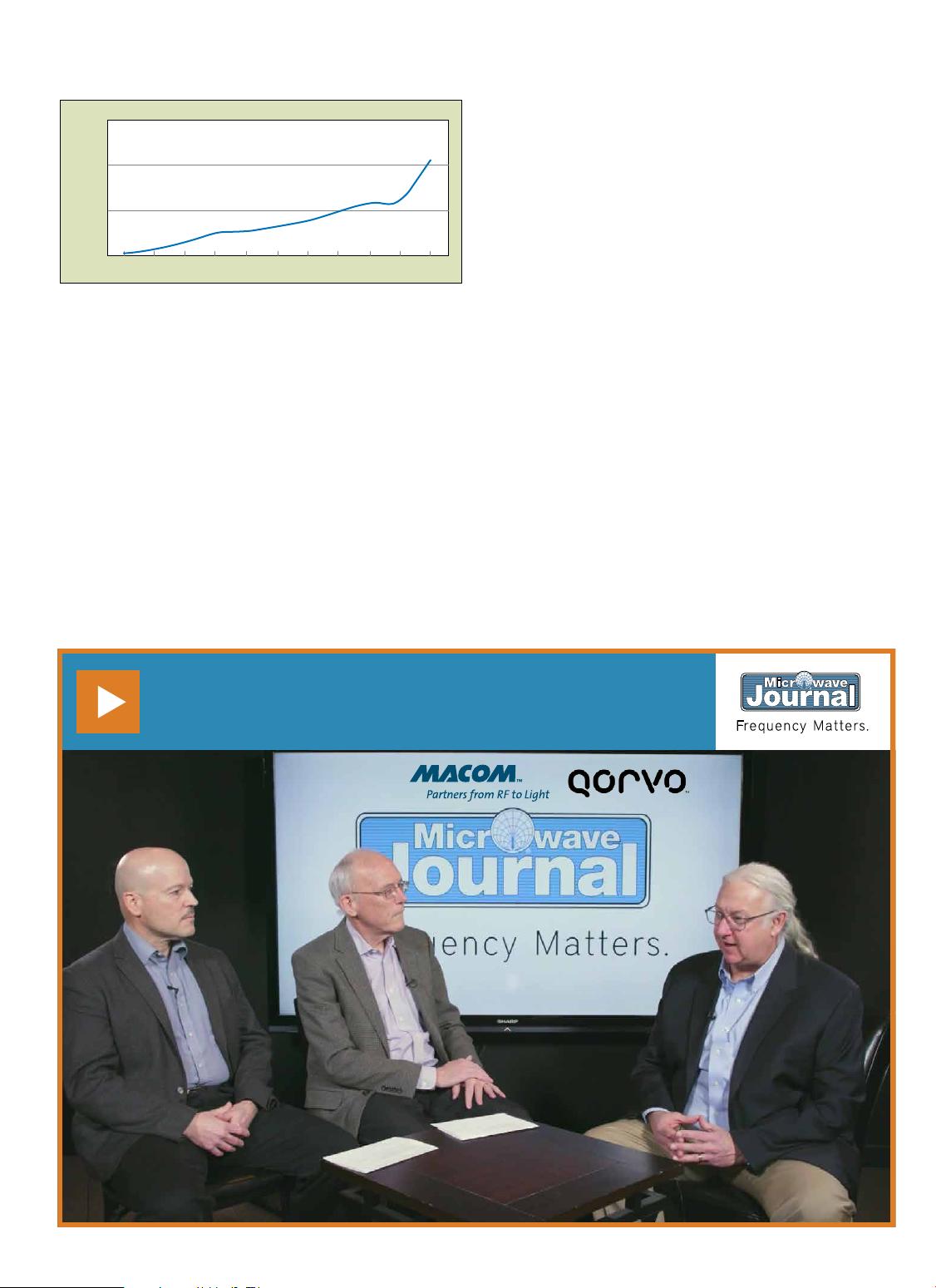

Strategy Analytics forecasts the global EW market will

grow to $20 billion by 2027 (see Figure 4). The associ-

ated market for semiconductors and other components

for RF-based EW systems will grow at a CAAGR of 8.4

percent through 2027. Future EW program will increas-

ingly use GaN, making this semiconductor technology

a staple ingredient in EW systems. This will be coupled

with requirements for direct and faster digital synthesis

of RF signals across the full frequency spectrum.

COMMUNICATIONS

Military communications operate under an umbrella

of heterogeneous networks that enable the provision

of interoperable voice, video and data services across

a global environment, segmented according to security

policies, transmission requirements and the individual

needs of the end user. In terms of the networked bat-

tlespace, this can be summarized as:

• Upper level networking, consisting of infrastructure

and networking components.

• Mid-level networking providing high capacity back-

haul.

• Support to the tactical edge for end-users and sensors.

Similarly, 5G serves as an aggregator technology that

encompasses a range of network types and technolo-

gies to serve traditional voice, video and data require-

ments to the end user, as well as enabling capabilities

for connectivity across devices, including vehicles, ma-

chines, sensors and devices.

Phased arrays, beamforming, mmWave frequencies,

SATCOM, GaN, duplex communications and shared

spectrum access are among the crossover technologies

that will become common across both commercial and

military communications.

Communicating voice, data and video simultane-

ously and securely over wider and higher bandwidths

in an increasingly complex spectrum environment will

underpin the trends in military communications system

design and supporting components, including software-

dened architectures, solid-state technologies such as

GaN, radio-satellite communications and integration

with wireless networks.

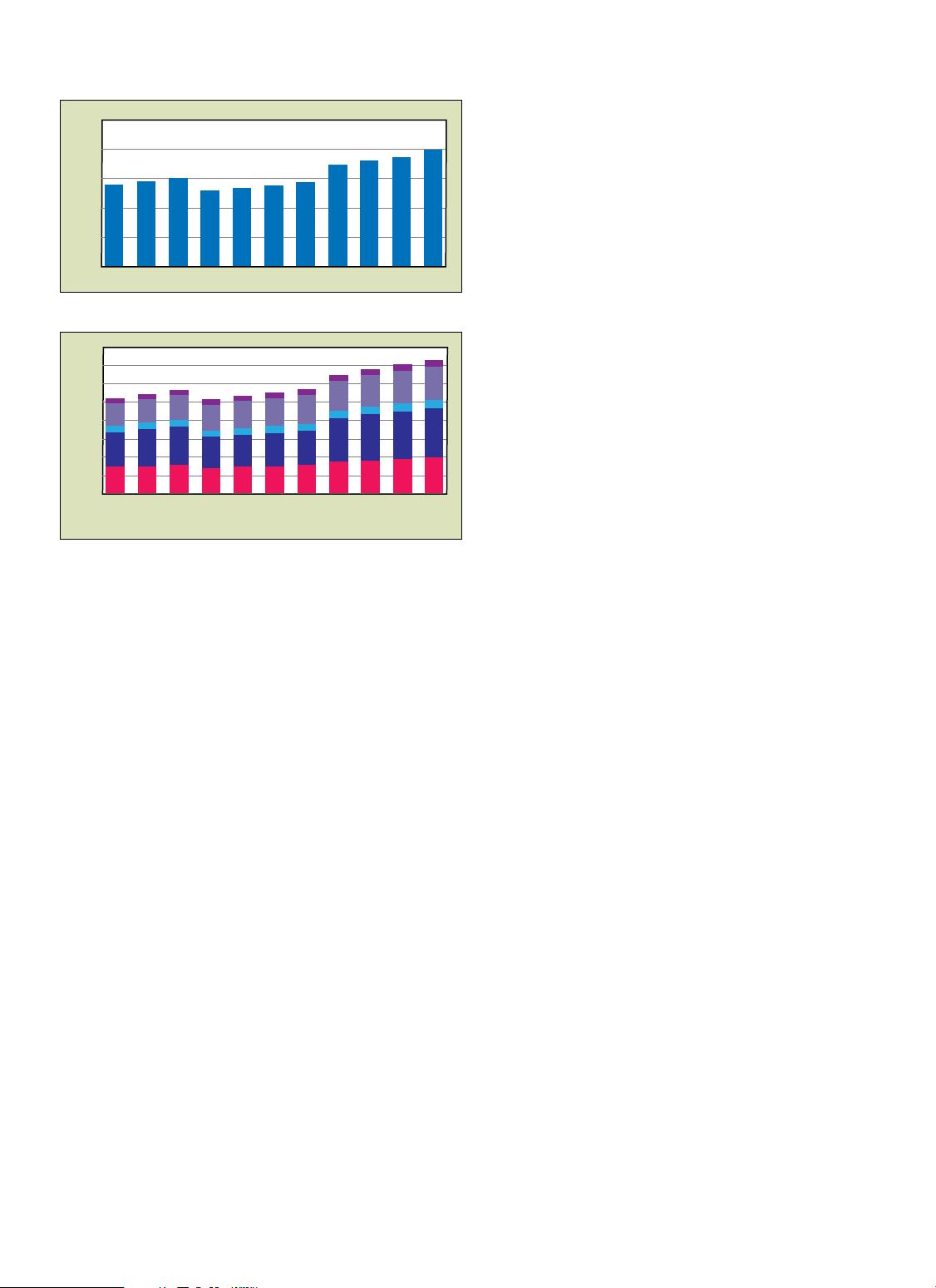

Strategy Analytics forecasts spending on global mili-

tary communications systems and services will grow to

over $36.7 billion in 2026, a compound annual growth

rate of 3.5 percent (see Figure 5).

RF GaN GROWTH

Demand from military radar, EW and communications

applications will provide the primary drivers for GaN

market adoption, and this will be coupled with ongoing

demand from the rollout of commercial wireless infra-

s Fig. 4 Global EW market forecast.

25

20

15

10

5

0

$ Billion

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

s Fig. 5 Global military communications market outlook, by

segment.

40

35

30

25

20

15

10

5

0

$ Billion

Radio SATCOM Datalink Network Other

2017 2018 2019 2020 2021 2022 2023 2024 2025 20262016

剩余30页未读,继续阅读

293 浏览量

102 浏览量

308 浏览量

2024-03-19 上传

193 浏览量

1159 浏览量

zzhou01

- 粉丝: 0

- 资源: 6

我的内容管理

展开

我的内容管理

展开

最新资源

- 先进算法讲义-中科大.pdf 需要的下吧

- TD-SCDMA Principle -李世鹤

- rhce5 启动引导troubleshooting实验笔记

- 软件体系结构(ppt版)

- C和C++嵌入式系统编程

- Java企业版中性能调节的最佳实践.pdf

- Log4j中文手册2006_04_07_205056_ZCxoePRlHJ_2.pdf

- AutoCADAutoCAD 2005中文版是美国AutoDesk公司推出的AutoCAD软件的最新版本,它在以前版本的强大功能之上又增加了新的功能。通过本章的学习,读者将对AutoCAD 2005中文版有一个整体上的了解,学会安装和启动的方法,初步了解AutoCAD 2005中文版的界面组成。

- 全国等级考试 二级vf机试题

- The Definitive Guide to Grails Second Edition

- LINUX电子书

- IGBT 应用系统资料!

- 单片机恒温箱温度控制系统的设计

- ARM的嵌入式系统硬件结构设计经典

- MATLAB偏微分方程工具箱简介

- TestLink1.7RC3使用说明书.doc