1. Limited policy certainty for LDES,

compounded by concurrent jurisdiction

While many regions note the strategic

importance of energy storage overall, there are

few concrete actions being taken to accelerate

the sector, let alone LDES within this broader

envelope. Moreover, in regions like the EU and

US, concurrent jurisdiction between different

levels of government (e.g., state vs. Federal in

the US, country vs. EU-level in Europe, and

state vs. central in India) can create additional

uncertainty and complexity to manage.

2. Limited awareness and definitions of the asset

class, leading to narrow technical taxonomy

for energy storage and lack of a defined

market and monetization opportunities

As an emergent class of technologies,

understanding of LDES solutions, their

attributes, and their value propositions to

customers and the power system is also

underdeveloped. The term energy storage tends

to be more narrowly defined to short duration

(commonly one to four hours of storage) and

conjures the traditional image of a containerized

lithium-ion or lead acid battery pack. Given

the high market share of lithium-ion systems in

today’s grid-scale stationary storage, most of the

technical requirements in power markets (e.g.,

roundtrip efficiency, safe operating parameters,

degradation, lifetime, cyclability) are defined

based on the performance characteristics of

these solutions and will need to be adapted

for LDES technologies that can deliver similar

services but with inherently different technical

and operating profiles. Similarly, in many markets

no distinction is made between conventional

pumped hydro and novel forms, such as

off-stream. This narrow definition of energy

storage also extends to customer technology

procurement, where existing Requests for

Proposals (RFPs) for energy storage projects

preclude novel solutions with different

characteristics. In some jurisdictions, LDES is

also considered as the same asset class as

electricity generation or transport, which can

lead to double taxation.

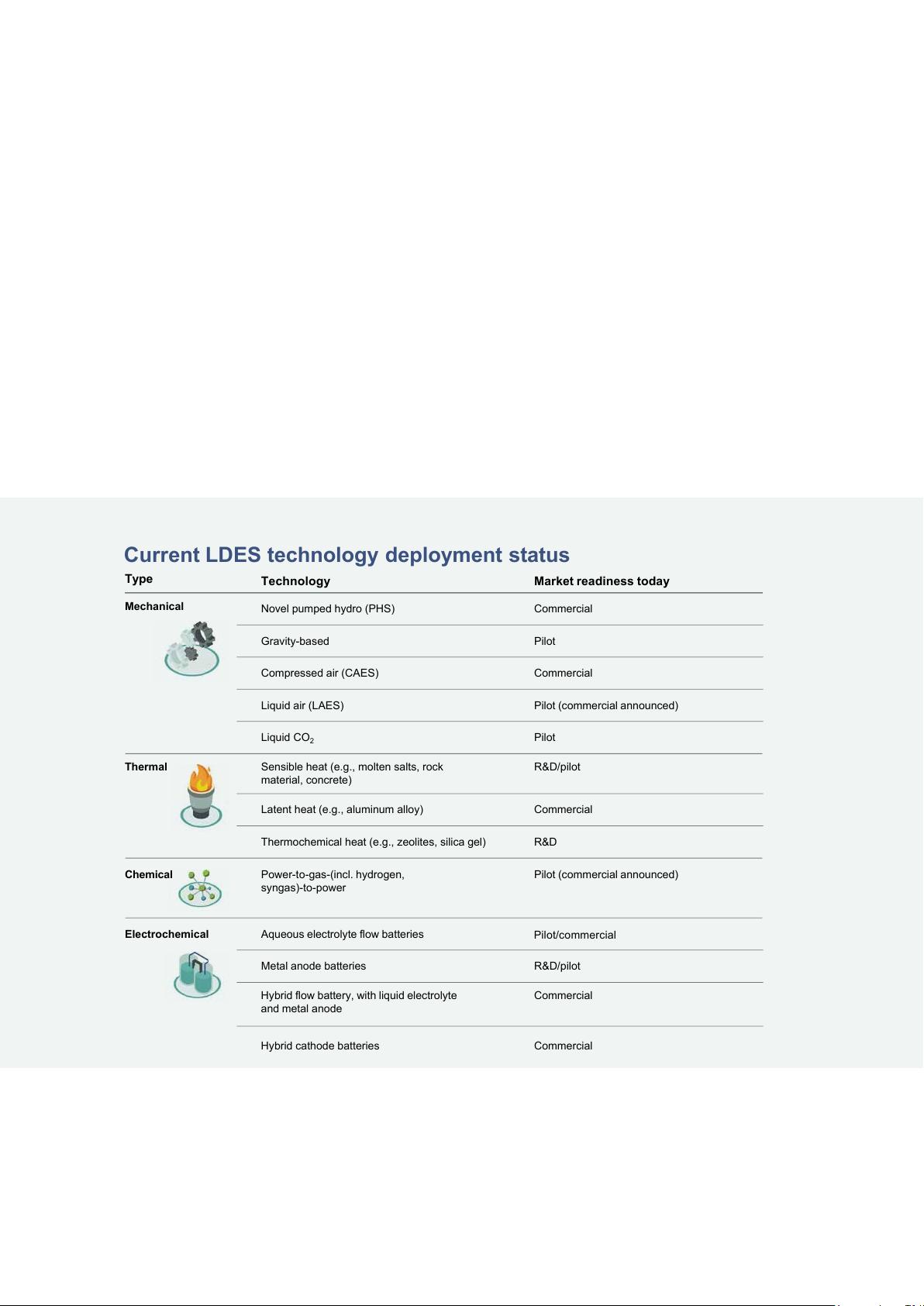

3. High initial project costs

8

due to limited

commercial scale and deployment history

Limited commercial deployment of LDES

solutions beyond first-of-a-kind (FOAK) projects

has resulted in high initial capex requirements

due to limited economics of scale in production

and procurement (refer to Exhibit 3 for high

level summary of LDES deployment status).

Elevated initial project costs in turn mean

lower economic competitiveness versus

other established forms of flexibility that have

achieved economies of scale.

4. Investor perception of increased project

risks leading to elevated rate of return

requirements

Project investors require a premium to cover

perceptions of higher risk associated with an

asset class with limited track record in the early

days of market formation. Although there are

applications (e.g., substitution of diesel power in

remote applications such as mining, or isolated

communities including islands) offering sufficient

Return on Investment (ROI) today, the majority of

LDES business cases cannot support elevated

capital cost requirements reflecting technology

risk. Additionally, some development banks find

it difficult to support LDES because few risk

assessments are available.

Barriers to LDES adoption

While there is considerable evidence to support the need for

LDES solutions as a part of the decarbonization equation,

there are several barriers to widespread deployment of LDES.

8 Costs of LDES systems are expected to decline significantly to 2040. Benchmarking by the LDES Council in 2021 suggested 60% and 25-50%

declines in power and balance of plant capex and energy capex from 2025 levels. Learning rates for LDES assets were estimated to be between

12-18%, comparable to those for other clean energy technologies.

15

The journey to net-zero | An action plan to unlock a secure, net-zero power system

我的内容管理

展开

我的内容管理

展开