汇丰银行全球农业商业:播下成长的种子-责任声明

需积分: 0 195 浏览量

更新于2023-11-22

收藏 2.19MB PDF 举报

《汇丰银行-全球农业商业:播下成长的种子》是一份50页的文件,介绍了汇丰银行在全球农业领域的经营情况和战略。本文对该文件进行总结及翻译如下:

《汇丰银行-全球农业商业:播下成长的种子-1-50页.pdf》总结

本文件是一份名为《汇丰银行-全球农业商业:播下成长的种子-1-50页.pdf》的文件。这份文件旨在介绍汇丰银行在全球农业领域的业务和战略。在这50页的文件中,提供了关于该银行的农业业务的详细信息。此外,文件还包含了适用的免责声明。

该文件揭示了汇丰银行在全球农业商业中所扮演的角色。作为一家全球性银行,汇丰银行一直致力于支持农业产业的发展。文件中介绍了该银行提供的农业金融产品和服务,以帮助农业相关企业实现可持续增长和成功。

文件的前几页提供了关于全球农业行业现状和趋势的概述。它提到了农业领域的挑战和机遇,以及汇丰银行对这些问题的应对策略。文件还介绍了该银行的全球农业团队,以及他们的专业知识和经验。

随后的几页详细介绍了汇丰银行的农业金融产品和服务。其中包括贸易融资、农业保险、农业投资和农业咨询等方面。汇丰银行通过这些产品和服务,为农业企业提供资金支持、风险管理和专业建议。

最后几页是免责声明,说明了该文件的信息的准确性和完整性,并提醒读者在做出任何决策前应自行核实信息。文件还强调了投资和决策所带来的风险,以及汇丰银行不对由此产生的任何损失负责。

总的来说,《汇丰银行-全球农业商业:播下成长的种子-1-50页.pdf》是一份介绍汇丰银行在全球农业领域的业务和战略的文件。文件提供了关于该银行农业金融产品和服务的详细信息,并附有免责声明。读者需要注意核实信息和承担决策风险。

EQUITIES

● AGRIBUSINESS

January 2019

8

How to play the sector

We prefer Buy rated OCI, CF Industries, Nutrien, and Mosaic in the fertilizer space; UPL

in crop chemicals. We think the earnings momentum of the sector coupled with cash

generation could possibly result in corporate actions including buyback announcements and

expansion plans.

Notably, Mosaic did not announce a buyback in 2018, unlike its peers, but may do so and/or

increase its dividend given the solid cash at disposal (we estimate 2019e FCF less dividends of

cUSD1bn). CF Industries completed share buybacks worth USD150m in 2018 and is planning

to complete the remaining USD350m authorized through 2020, although we expect the

company could achieve its target well in advance as management believes that CF shares

could offer more return currently than growth through expansion.

The scope and quantum of further buyback announcements by Nutrien (in addition to USD1.6bn

already completed in 2018) will likely depend upon its potential acquisition pipeline in Brazil. Notice

that Nutrien has an open Normal-Course Issuer Bid (NCIB) offer for 3% of shares (cUSD950m) by

February 2019, but also has USD1.5bn debt maturing in 1Q 2019, which the company plans to

repay through the USD4bn gross proceeds from the sale of SQM shares in 4Q 2018.

For OCI, we expect the ramp-up of new plants combined with historically low capex to generate

high free cash flow and thus drive rapid balance sheet de-leveraging and improvement in returns.

We estimate OCI can reduce group debt from USD4.3bn in 2018e to just USD2.5bn by end-2020e.

UPL’s share price has been affected by an overhang caused by the Arysta acquisition and

other issues including FX impact and US-China trade wars. We believe even part delivery on

synergies from the Arysta acquisition would have the twin impact of: 1) increasing earnings; and

2) expanding valuation multiples. There could be a positive surprise to earnings and multiples

from any good news related to the trade war or currency movements.

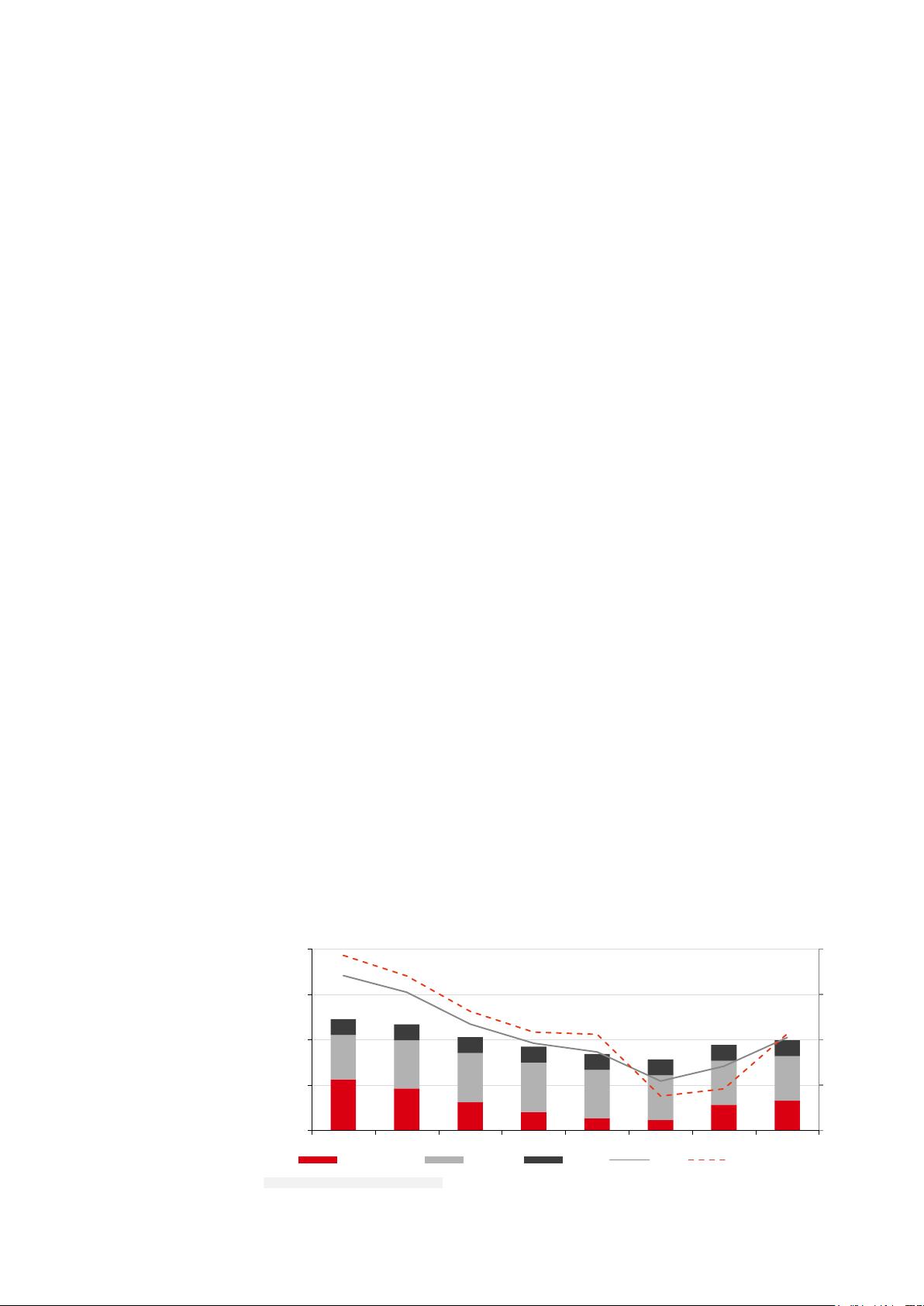

The fallout of a cold Fall

According to CRU reports, the cold Fall weather in the US severely affected 4Q 2018 fertilizer

application. The impact was likely more profound for retail and nitrogen businesses, implying

that NTR and CF will be the most affected in our coverage.

Weather-related disruptions are not uncommon in agriculture and usually result in a rebound in the

following application window. Hence, we expect a catch-up in 1H 2019, as was the case in 2Q

2018. In fact, the mix shift towards urea/UAN turned out to be positive for nitrogen sales at that time.

However, the key downside risk is the potential impact of the El Nino weather pattern on fertilizer

application and crop prices. The World Meteorological Organization (WMO) predicts a 75-80%

probability of El Nino conditions by February 2019, although this is not expected to be as severe

as the 2015-2016 event. In the event of El Nino causing a widespread drought, fertilizer

application could be impacted, resulting in downside risk to our earnings forecasts. We plan to

elaborate on the potential impact of El Nino in a separate report to be published in the future.

That said, we see 4Q 2018 earnings for US companies gravitating towards the lower end of

guidance. This coupled with investor cautiousness towards prolonged weather-related risks and

the impact of tariffs could result in some negative sentiment. Nonetheless, we see value in

fertilizer stocks, exacerbated by the recent decline in share prices.

Weather affects sentiment

more than earnings;

expected rebound in sales

will likely depend upon the

severity of El Nino

剩余49页未读,继续阅读

2023-07-26 上传

2021-09-03 上传

255 浏览量

181 浏览量

191 浏览量

156 浏览量

140 浏览量

2024-10-28 上传

icwx_7550592

- 粉丝: 20

- 资源: 7163

我的内容管理

展开

我的内容管理

展开

最新资源

- PIC24FJ64GA004

- 30秒清除你电脑中的垃圾(使你电脑急速如飞)

- 基于NS2无线传感网路由协议模型的设计与研究

- MATLAB 图像处理命令

- GCC中文用户手册(PDF)

- 架构风格与基于网络的软件架构设计

- c与c++嵌入式系统编程

- 8051单片机指令系统

- 开发JavaScript程序最优秀的IDE

- Microsoft Windows Internals

- VIM7.2中文用户手册

- 嵌入式笔记开发入门、入门经典

- 键盘的应用-按键上每个键的作用

- java自考大纲试验代码

- 解决checkstyle出现的问题:Got an exception - java.lang.RuntimeException Unable to get class information for Exception

- java执行系统命令