XLoss:不确定源下机会性频谱接入的带宽混合选择策略

64 浏览量

更新于2024-08-28

收藏 938KB PDF 举报

在认知无线电网络中,主要服务提供者(PSP)为了经济利益设定空闲授权频谱的价格并进行销售或租赁。而次要服务提供者(SSP)作为机会性频谱接入(OSA)的支持者,可以从PSP处购买或租用频谱来满足自身用户(SU)的需求。然而,由于PSP服务的不可预测性,SSP面临着金钱风险和可能无法满足SU流量需求的挑战。在这种环境下,如何衡量OSA的风险、选择合适的频谱组合(band-mix),以及在多个空闲频谱中合理分配流量是一项复杂的问题。

本文提出了一个名为“X损失”(The X Loss)的概念,这是一个直观的风险度量指标,用于评估SSP在OSA中的潜在风险。尽管X损失因其简洁性而吸引人,但它存在两个主要问题:首先,它低估了OSA的实际风险;其次,从数学角度看,X损失是非可加性的,这使得在进行流量分担时,支持基于band-mix的选择变得困难。因此,X损失在实际操作中可能存在局限性,不能准确反映复杂环境中频谱利用的风险和效益。

为了克服这些问题,作者提出了一种改进的方法,旨在解决在不确定的频谱供应下,如何有效地进行band-mix选择和流量分配。这可能包括开发更精确的风险评估模型,考虑多种不确定性因素,如频谱占用率变化、交易时间窗口、市场动态等。此外,可能还会涉及到优化算法的应用,如线性规划或动态规划,以找到在风险和收益之间平衡的最佳频谱组合策略。

文章的核心内容可能涉及以下几点:

1. **X损失的定义与局限**:介绍X损失如何计算,以及它如何低估风险,并解释其非可加性对band-mix决策的影响。

2. **风险建模与修正**:探讨如何构建更全面的风险模型,考虑更多的不确定性因素,以便提供更准确的预期风险评估。

3. **流量分配策略**:讨论如何在多频谱环境中设计有效流量分担策略,以最大化收益并控制风险。

4. **算法设计与优化**:可能会介绍特定的算法,如遗传算法、模拟退火或其他动态规划方法,用于在band-mix选择中求解最优化问题。

5. **实证分析与案例研究**:通过实验数据或实际案例展示X损失修正后的band-mix选择方法在实践中的性能和有效性。

这篇论文针对认知无线电网络中的频谱管理问题,提出了一种新的风险度量工具,并探讨了如何结合这一工具进行更有效的band-mix选择和流量分配,以降低不确定性带来的挑战。这对于理解和优化OSA在实际环境中的部署具有重要的理论和实践价值。

The rest of the paper is organized as follows: In Section 2,

we describe the roles of the PSPs and the SSP in the

spectrum trading and define the reward function for the

SUs as well as the risk function for OSA. We introduce

related concepts to band-mix selection including band-mix

selection rule, efficient OSA curves and the SSP’s utility

function in Section 3. We elaborate on the two proposed

risk metrics for OSA: the X loss and the expected X loss in

Section 4. With the discritized version of the expected X

loss, we illustrate the optimal band-mix selection of the SSP

for OSA in Section 5. Finally, we cond uct numerical

simulations and analyze the performance results in Sec-

tion 6, and draw the concluding remarks in Section 7.

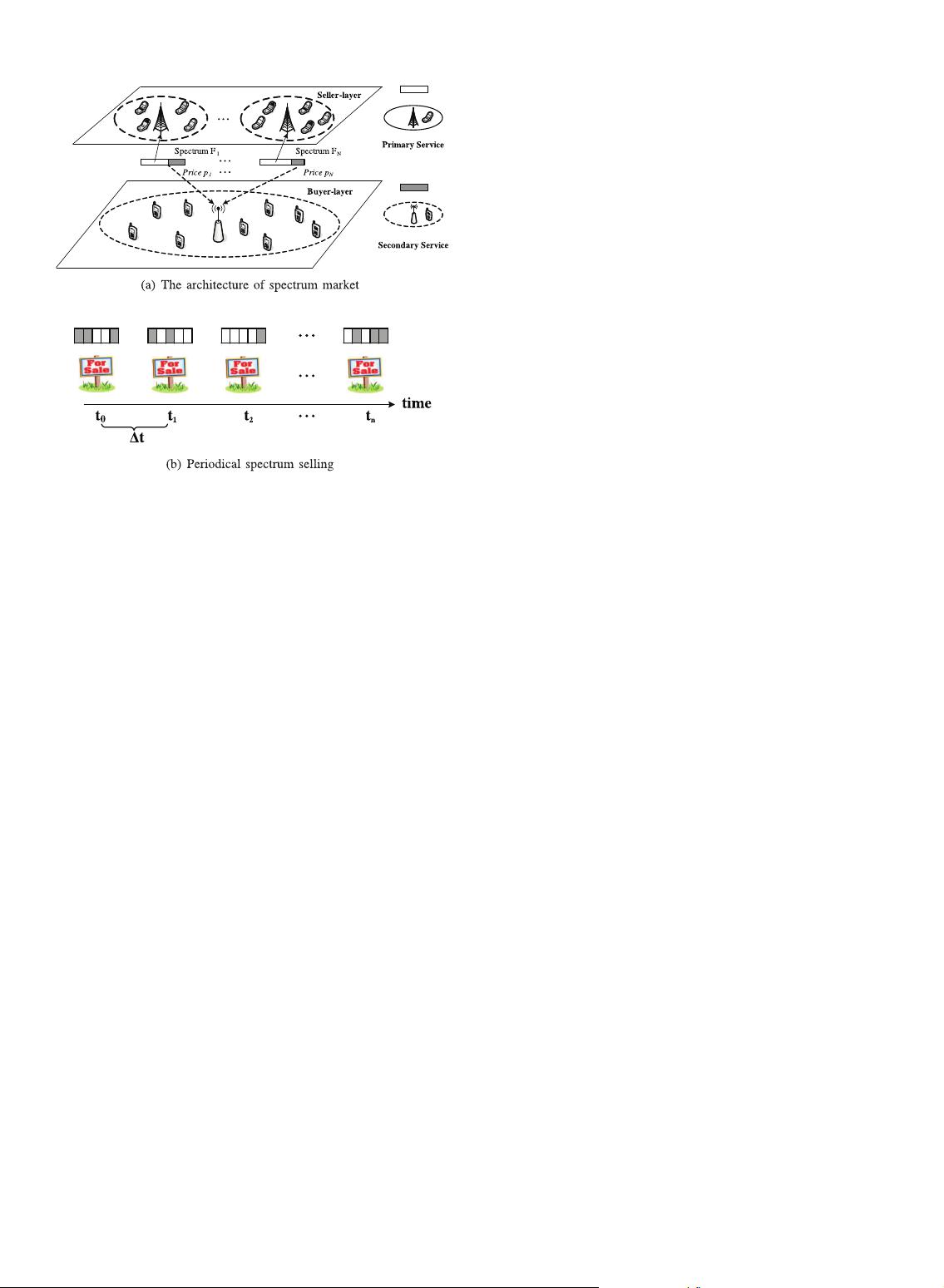

2SYSTEM MODEL

2.1 Spectrum Market

We consider a spectrum market in cognitive radio networks

[16] with multiple PSPs operating on different spectrum

bands and a SSP who serves a group of SUs as shown in

Fig. 1a. The SUs can take opportunistic use of these licensed

spectrum bands when the primary services are not on, but

must evacuate from these bands immediately when

primary services become active. In addition, we assume

all the spectrum transactions take place at starting time of

each period

3

as shown in Fig. 1b, and the payment for

spectrum trading is nonrefundable.

In this case, PSPs will set reasonable prices for the

unoccupied bands considering the quality of the bands as

well as competition among the PSPs in the spectrum market

[13], [15], [16], and sell those bands periodically for

monetary gains. Correspondingly, if the SSP (e.g., the base

station (BS) or the access point (AP)) realizes there is not

enough radio resource for the traffic demands of its SUs,

the SSP will play the role of trading agent for the SUs [6].

Specifically, the SSP will try to select a mix of currently

vacant licensed bands, buy those bands from the PSPs,

charge the SUs with the prices set by PSPs and share the

bands purchased among multiple SUs in a time-division

multiple access (TDMA) manner.

2.2 SSP’s Revenue and Risk Function

Assume there are n available spectrum bands owned by

different PSPs with identical bandwidth, which is equal to

1, within the sensing range of the SSP. Considering the

unpredictable activities of primary services, the uncertain

spectrum supply of different bands for a given period is

represented by ss ¼ðs

1

;s

2

; ...;s

n

Þ, where s

i

is a random

variable

4

within the domain of ½0; 1. Suppose, the total

traffic demand from the SUs is 1, and the proportional

composition of the band-mix that the SSP picks up is

!! ¼ð!

1

;!

2

; ...;!

n

Þ, !! 2W, where

P

n

i¼1

!

i

¼ 1. Then, the

total spectrum resources the SSP can obtain is

P

n

i¼1

s

i

!

i

,

and the expected reward for the SSP can be written as

ð!!Þ¼r

X

n

i¼1

IE ½s

i

!

i

; ð1Þ

where r is a constant, representing the SSP’s reward for

satisfying one unit of traffic.

5

Correspondingly, the risk

function of the SSP can be expressed as

‘ð!!; ssÞ¼pp

T

!! rss

T

!!; ð2Þ

where pp ¼ðp

1

;p

2

; ...;p

n

Þ is the charging price vector set by

the PSPs for OSA per period, and p

i

is a constant during a

spectrum trading period. Note that p

i

p

j

,ifIE ðs

i

ÞIE ðs

j

Þ.

Since r is a fixed number and ss is a random vector, the risk

for OSA depends on both the statistical characteristics of ss

and the SSP’s selection of bands belonging to the PSPs.

3PRIMARY CONCEPTS FOR BAND-M IX SELECTION

3.1 Band-Mix Selection Principle

Intuitively, the SSP is able to maximize his revenue by

pouring all the traffic of SUs over a particular band with the

maximal expected reward. However, the risk of using that

band may be quite high. A rational or risk-averse SSP is not

likely to gamble all the traffic on one band since the reward

may be extraordinarily low considering the activities of

primary services.

Therefore, the expected reward should not be the only

criterion in choosing the spectrum bands to access; instead,

the risk of the reward must be considered by the SSP. It is

reasonable to believe that if any two band-mixes have the

same expected reward, the SSP will prefer the one having

the smaller risk for OSA, and if any two band-mixes have

the same risk, the SSP will prefer the one having the greater

expected reward. So, the criterion for band-mix selection is

as the follows.

PAN ET AL.: THE X LOSS: BAND-MIX SELECTION FOR OPPORTUNISTIC SPECTRUM ACCESSING WITH UNCERTAIN SPECTRUM SUPPLY... 2135

Fig. 1. System model for spectrum trading.

3. The selling/buying period 4t should not be too long (e.g., days,

months, or years) to make dynamic spectrum access infeasible, and it

should not be too short (e.g., milliseconds or seconds) to incur over-

whelming overhead in spectrum trading. The typical duration is minutes or

hours as shown in [32]. In the rest of paper, we assume that all the spectrum

transactions are of fixed duration, so that the time parameter is not included

in our formulation.

4. Here, s

i

can be interpreted as unoccupie d time or unoccupied

bandwidth by primary services for band i during one time period.

5. With the assumption that r is fixed, ð!!Þ can also be interpreted as the

expected traffic demands that the SSP is able to support.

剩余11页未读,继续阅读

点击了解资源详情

点击了解资源详情

点击了解资源详情

2021-02-08 上传

2021-02-10 上传

2021-02-11 上传

2021-02-09 上传

2021-02-10 上传

2021-05-29 上传

weixin_38517113

- 粉丝: 3

- 资源: 888

我的内容管理

展开

我的内容管理

展开

最新资源

- C语言数组操作:高度检查器编程实践

- 基于Swift开发的嘉定单车LBS iOS应用项目解析

- 钗头凤声乐表演的二度创作分析报告

- 分布式数据库特训营全套教程资料

- JavaScript开发者Robert Bindar的博客平台

- MATLAB投影寻踪代码教程及文件解压缩指南

- HTML5拖放实现的RPSLS游戏教程

- HT://Dig引擎接口,Ampoliros开源模块应用

- 全面探测服务器性能与PHP环境的iprober PHP探针v0.024

- 新版提醒应用v2:基于MongoDB的数据存储

- 《我的世界》东方大陆1.12.2材质包深度体验

- Hypercore Promisifier: JavaScript中的回调转换为Promise包装器

- 探索开源项目Artifice:Slyme脚本与技巧游戏

- Matlab机器人学习代码解析与笔记分享

- 查尔默斯大学计算物理作业HP2解析

- GitHub问题管理新工具:GIRA-crx插件介绍