探索计算机组成原理:历史、设计与技术趋势

需积分: 34 117 浏览量

更新于2024-07-27

1

收藏 4.82MB PDF 举报

《计算机组成原理》英文版是一本深入探讨现代计算机设计基础和技术趋势的教科书。该书首先在第一章“Fundamentals of Computer Design”中介绍了计算机设计师的角色,他们肩负着将先进技术转化为实用、高效的计算设备的任务。章节1.2详述了这个任务,强调了设计者需理解和掌握如何平衡性能、成本和易用性。

随着时代的进步,1.3节讲述了技术与计算机使用趋势之间的关系,指出半个世纪以来,计算机技术经历了翻天覆地的变化,存储程序计算机的发展为现代个人电脑奠定了基础。作者通过对比1945年和1965年的技术水平,突显了技术进步的速度和规模。

1.4和1.5部分重点关注成本问题,讨论了随着时间推移,硬件成本的下降以及衡量和报告性能的标准变化。这些章节有助于读者理解技术进步如何影响计算机系统的性价比。

在关键的1.6章,“Quantitative Principles of Computer Design”,作者深入讲解了计算机设计中的量化原则,如处理器速度、内存容量和能效等核心概念,这些都是决定系统效能的关键因素。

第1.7章引入了“Memory Hierarchy”概念,这是计算机架构中的重要组成部分,它解释了为何不同层次的存储器(如寄存器、缓存、主存和硬盘)被设计成有层次结构,以优化数据访问速度和存储效率。

1.8节则揭示了设计过程中可能出现的误解和陷阱,提醒读者在追求性能提升时需要注意的问题。这部分内容对避免设计误区至关重要。

1.9“Concluding Remarks”总结了前面章节的主要内容,并展望了未来可能的发展方向,同时提供了历史视角和参考文献,帮助读者将当前知识置于更广阔的背景中。

最后,附录的“Exercises”提供了实践性的学习机会,鼓励读者通过解决实际问题来巩固理论知识,确保了理论与实践的紧密结合。

《计算机组成原理》英文版是一本既涵盖了技术变迁又注重设计原则的教材,对于理解计算机硬件和系统设计的发展脉络,以及如何在这个快速发展的领域保持创新和效率具有重要价值。

1.4 Cost and Trends in Cost

15

before it becomes price, and the computer designer should understand how a de-

sign decision will affect the potential selling price. For example, changing cost

by $1000 may change price by $3000 to $4000. Without understanding the rela-

tionship of cost to price the computer designer may not understand the impact on

price of adding, deleting, or replacing components. The relationship between

price and volume can increase the impact of changes in cost, especially at the low

end of the market. Typically, fewer computers are sold as the price increases. Fur-

thermore, as volume decreases, costs rise, leading to further increases in price.

Thus, small changes in cost can have a larger than obvious impact. The relation-

ship between cost and price is a complex one with entire books written on the

subject. The purpose of this section is to give you a simple introduction to what

factors determine price and typical ranges for these factors.

The categories that make up price can be shown either as a tax on cost or as a

percentage of the price. We will look at the information both ways. These differ-

ences between price and cost also depend on where in the computer marketplace

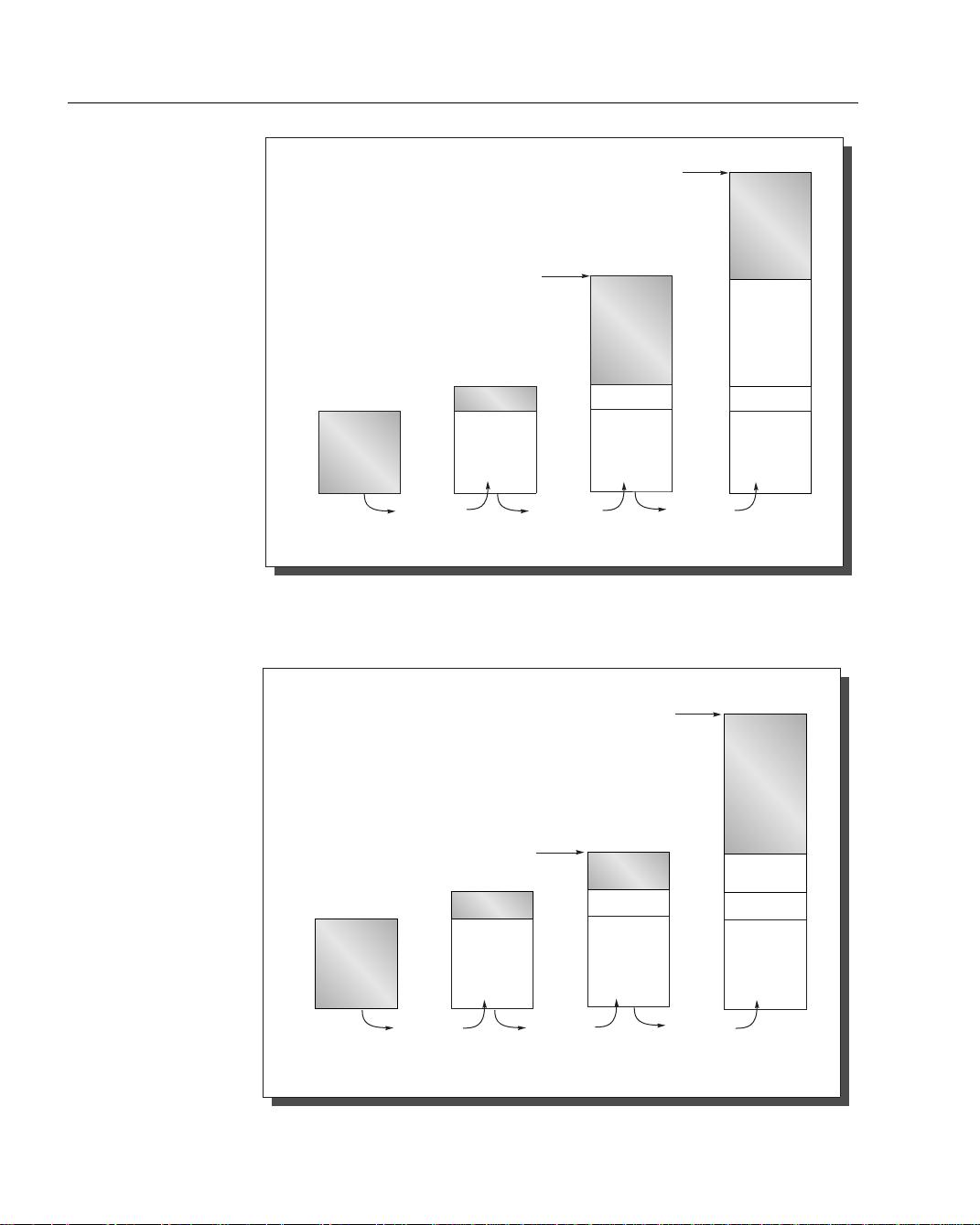

a company is selling. To show these differences, Figures 1.7 and 1.8 on page 16

show how the difference between cost of materials and list price is decomposed,

with the price increasing from left to right as we add each type of overhead.

Direct costs

refer to the costs directly related to making a product. These in-

clude labor costs, purchasing components, scrap (the leftover from yield), and

warranty, which covers the costs of systems that fail at the customer’s site during

the warranty period. Direct cost typically adds 20% to 40% to component cost.

Service or maintenance costs are not included because the customer typically

pays those costs, although a warranty allowance may be included here or in gross

margin, discussed next.

The next addition is called the

gross margin

, the company’s overhead that can-

not be billed directly to one product. This can be thought of as indirect cost. It in-

cludes the company’s research and development (R&D), marketing, sales,

manufacturing equipment maintenance, building rental, cost of financing, pretax

profits, and taxes. When the component costs are added to the direct cost and

gross margin, we reach the

average selling price—ASP in the language of

MBAs—the money that comes directly to the company for each product sold.

The gross margin is typically 20% to 55% of the average selling price, depending

on the uniqueness of the product. Manufacturers of low-end PCs generally have

lower gross margins for several reasons. First, their R&D expenses are lower.

Second, their cost of sales is lower, since they use indirect distribution (by mail,

phone order, or retail store) rather than salespeople. Third, because their products

are less unique, competition is more intense, thus forcing lower prices and often

lower profits, which in turn lead to a lower gross margin.

List price and average selling price are not the same. One reason for this is that

companies offer volume discounts, lowering the average selling price. Also, if the

product is to be sold in retail stores, as personal computers are, stores want to

keep 40% to 50% of the list price for themselves. Thus, depending on the distri-

bution system, the average selling price is typically 50% to 75% of the list price.

剩余911页未读,继续阅读

255 浏览量

104 浏览量

2024-12-29 上传

2011-06-07 上传

4333 浏览量

199 浏览量

YALE_XYZ

- 粉丝: 0

我的内容管理

展开

我的内容管理

展开

最新资源

- NodeBB插件:IP.Board数据导入解决方案

- Pico主题发布:Ghost付费会员功能的免费开源方案

- JS实现画报图片展示与相册切换特效

- 全屏模式Android选择控件DirectSelect使用教程

- SMastroianni网站构建与部署流程解析

- 实现跨社交平台的数据提交方法

- gostatus:查看Go库状态的命令行工具

- 高端鞋履商城响应式网站完整代码包下载

- QUaModbusClient:实现Modbus与OPC UA之间的转换

- Nimbella插件扩展Netlify站点的可移植无服务器API功能

- 探索GUI图形用户界面编程的奥秘

- 马赛克过渡焦点图切换特效实现与自动播放功能

- 手写数字识别的PCA算法实现方法及步骤

- Laravel框架下开发的实习生缺勤管理程序介绍

- JQuery完美弹出层插件:跨平台使用便捷指南

- GitHub Pages:个人网站的Markdown内容维护和预览