美元稳定币Tether的背后:690亿美元的问题

版权申诉

170 浏览量

更新于2024-07-11

收藏 33.57MB PDF 举报

"Bloomberg Businessweek - 11.10.2021" 是一份包含多个领域的财经新闻和分析的杂志,其中包括了科技、金融、商业和环境等方面的内容。

1. 特写(Features):

- 标题:“The $69 Billion Question”探讨的是Tether这种稳定币的问题。每枚Tether稳定币都声称由美元支持,但文章可能深入研究了这些巨额资金的真实去向,以及其背后的透明度和潜在风险。

- 另一特写讨论了“Southwest Louisiana's Climate Exodus”,关注因飓风灾害导致的居民外流,以及天然气工人的涌入,这涉及气候变化、能源行业和人口迁移的复杂关系。

2. 短篇新闻(IN BRIEF):

- Volvo准备进行IPO,可能涉及到汽车行业的市场前景和公司估值。

- 中国房地产市场的更多担忧,可能提到了房地产泡沫、调控政策和市场稳定性。

3. 观点(OPINION):

- 文章指出华盛顿特区的工作力量需要减少任命并增加专业人士,这可能涉及政府机构效率和公共政策的话题。

4. 议程(AGENDA):

- 大银行的收益报告,反映了银行业的财务状况和经济复苏的迹象。

- G-20企业的税收会议,可能涉及国际税收改革,尤其是跨国公司税率的统一问题。

5. 言论(REMARKS):

- 金融应用程序为银行业带来了便利和趣味性,但同时也带来了风险,讨论了金融科技的发展与挑战。

6. 商业(BUSINESS):

- 企业客户对精英律师事务所的多样性施加压力,可能涉及法律服务行业的多元化和包容性议题。

- 电动汽车革命可能会绕过密歇根州,揭示了汽车产业转型中地域发展的不均衡。

7. 科技(TECHNOLOGY):

- 创业公司在气候数据收集方面引领太空竞赛,揭示了科技在环保和气候研究中的新角色。

- 一位告密者的计划,旨在创建一个更安全的Facebook,可能涉及社交媒体的隐私、安全和监管问题。

- Salesforce推出流媒体服务,展示了软件巨头如何拓展业务领域。

8. 金融(FINANCE):

- 当前是投资的好时机,可能分析了市场状况和投资策略。

这期《彭博商业周刊》提供了丰富的财经信息,包括稳定币的透明度、气候变化下的社会动态、科技公司的社会责任、金融市场动态等多个焦点话题,对于理解全球经济形势和行业趋势具有很高的价值。

11

REMARKS Bloomberg Businessweek October 11, 2021

Fintech companies that passed the

test presented by the pandemic have

seen their valuations soar

Money and data travel at warp speed, compressing space

and time, with less need for human intervention and more

demand for products to manage the ow. In the minds of

techies, this is a revolution in inclusion and democratization

for those left behind by thcentury banks. Fair enough: If

the best tech is like magic, banking hasn’t been magical for

some time. Startups are clearly better at ginning up eciency

through innovation.

But when instant gratication meets people’s pocket-

books, risks start to sneak in. Buy now, pay later programs

get more people to buy more things, but data in Australia

found in users paying late fees after missing repayments—

hardly a boon for equality. Robinhood Markets Inc., the

enabler for Reddit-fueled day traders, was ned million

by the Financial Industry Regulatory Authority over mislead-

ing information and weak trading controls. The war for cus-

tomers means ntech rms lend to people more likely to

default, one study found.

Fintech rms’ use of data and models may also have bene

-

ted from the lack of a long economic downturn. “Risks associ-

ated with lending haven’t been tested,” says former hedge fund

manager Marc Rubinstein. Federal Deposit Insurance Corp.

data show that from to there were U.S. bank

failures, but only since . And in a world where technol-

oy is winner-take-all, the algorithms that drive ntech suc-

cess could start to feel as exclusionary as the banks they seek

to replace. Their power is already being blamed for pushing up

home prices and discriminating against women and minorities.

This all adds up to a regulatory headache as governments

struggle to hold the reins of a sector that’s growing fast and

oers plenty of reward but also plenty of risk. The Covid-

pandemic coincided with headline-grabbing ntech failures—

payments rm Wirecard AG and supply chain nance company

Greensill Capital—where red ags went unnoticed. The job of

having to beef up rules after each crisis isn’t made easier by

politicians calling on the tech sector to keep churning out uni-

corns to boost jobs. “When it comes to regulation, I worry,”

says economist Eswar Prasad, a Cornell professor and author

of The Future of Money. Regulators “seem to get overtaken by

rapid developments.”

Fintech’s disruptive potential was unleashed in mature

markets such as the U.S. only recently, thanks to a conuence

of factors: low interest rates, better technoloy, rising con-

sumer demand, and a more permissive attitude toward non-

bank nance. Eciency gains in software have kept products

coming. The relentless march of e-commerce has boosted

demand for new ways to pay. And venture capital is the fuel:

Global VC funding in ntech reached a record .billion

in the rst half of this year, according to KPMG. Since ,

ntech has raised trillion in equity.

All that money pressures startups to keep growing at

breakneck speed—and explains the shift from plain-vanilla

payments products to more heavily regulated nancial activ-

ities, according to Victor Basta, chief executive ocer of

investment bank DAI Magister. Regular bank accounts don’t

keep people swiping, unlike the stu keeping users awake at

night: crypto trading, investing, shopping, and loans.

The pandemic was a key moment for the sector, as more

people were forced to turn to their smartphones for essen-

tials (government benets and savings) and not-so-essentials

(storming the barricades of GameStop Corp.). The ntechs

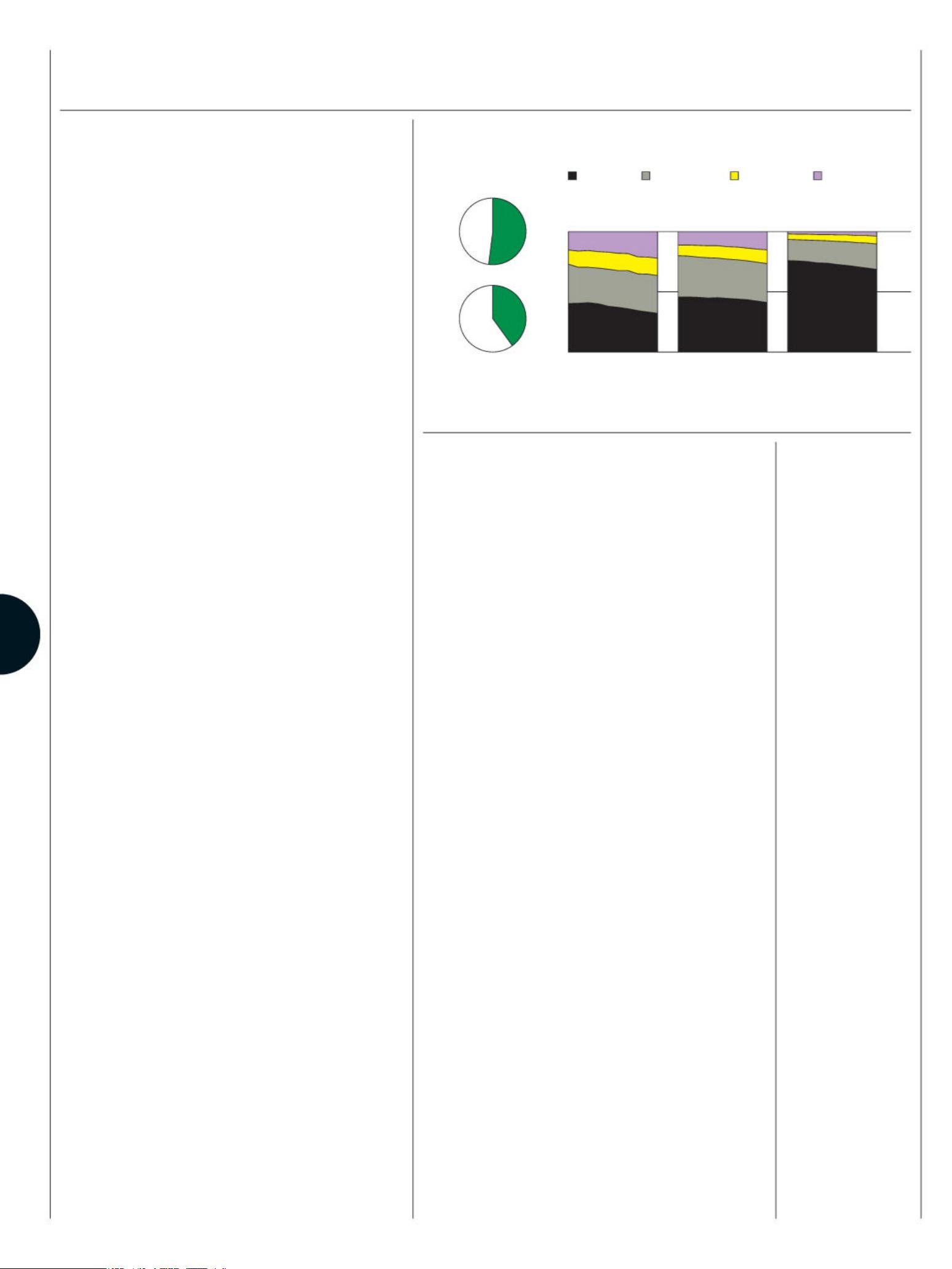

that passed the test have seen their valuations soar: Stripe

(billion), Klarna (.billion), Revolut (billion), and

Nubank (billion) rank among the most valuable pri-

vately owned unicorns in the world. On the stock market,

PayPal is worth billion, Square billion, and Adyen

billion (billion).

Traditional banks have been playing defense but also strik-

ing deals. Banks are one of ntech’s big funding sources:

Goldman Sachs Group Inc. and Citigroup Inc. participated in

and ntech deals, respectively, from to . Some

startups have chosen to become licensed banks themselves,

while big tech companies encroach into nancial territory

from the other direction: Amazon.com Inc. oers payments,

credit, and insurance with partner rms.

And the complexity of nancial regulation has opened

doors for tech startups. Some have exploited rules such as the

Durbin Amendment, which allows smaller banks to make more

money from card payments. Others have proted from laws

intended to improve competition, such as European Union

rules giving ntech companies access to bank account data.

The stunning collapse of Wirecard shows how easy it can

be to run rings around regulators. Here was a German bank

with access to deposits, a U.K.-regulated e-money institution,

and a payments rm on Visa Inc.’s and Mastercard Inc.’s net-

works, yet nobody acted on the red ags.

China—which had a head start on the U.S. and Europe in

ntech, thanks to years of cultivating revolutionary platform

companies such as Alibaba and Tencent—is likely the country

to watch. After a string of ntech scandals in the mid-s, the

government is cracking down on the platforms for perceived

monopolizing of sensitive data and hindering fair competition.

Governments have to do more to reduce the risks while

amplifying the benets of ntech innovation. Stronger

consumer protection and improvements to nancial liter-

acy would help. Regulators are also trying a more active

approach to technoloy, oering sandbox-type controlled

environments where ntech rms can experiment and grow.

But it’s hard to escape the feeling that a lot of the risks com-

ing down the pike are unpredictable and many-headed and

that regulators won’t keep up. With central bankers deter-

mined not to be disrupted in their management of the econ-

omy, perhaps another line from Hamlet will prove prescient:

“Neither a borrower nor a lender be.”

剩余75页未读,继续阅读

点击了解资源详情

点击了解资源详情

178 浏览量

2021-11-13 上传

171 浏览量

2021-11-14 上传

网络研究观

- 粉丝: 1w+

我的内容管理

展开

我的内容管理

展开

最新资源

- 在MFC状态栏中实现图片加载功能

- Foodly膳食计划应用:整合日历、购物与食谱管理

- 实现用户授权注册功能的React API全解

- POS平台阿拉伯语显示方法研究

- 软件评测师教程分享:帮助提升评测技能

- Delphi开发者的福音:NativeExcel快速生成Excel文件

- 素材天堂1.0绿色免费版 - 便捷的电脑端素材下载器

- 心力衰竭预测模型与数据分析报告

- 使用PHP MVC和SQLite创建用户CRUD系统教程

- 双轴模拟太阳敏感器光电组件的技术突破

- 使用JavaScript动态生成具有动态列数的表格

- 体验版音频转换工具的试用攻略

- 分享Apache CXF 2.7.6源代码包下载难题解决方案

- 映美FP580K打印机官方驱动 v2.2版下载

- ImageBox V7.9.0:批量下载网页图片的官方最新版

- Pandas库概述与数据处理实践