CHAPTER 1

Introduction

Practice Questions

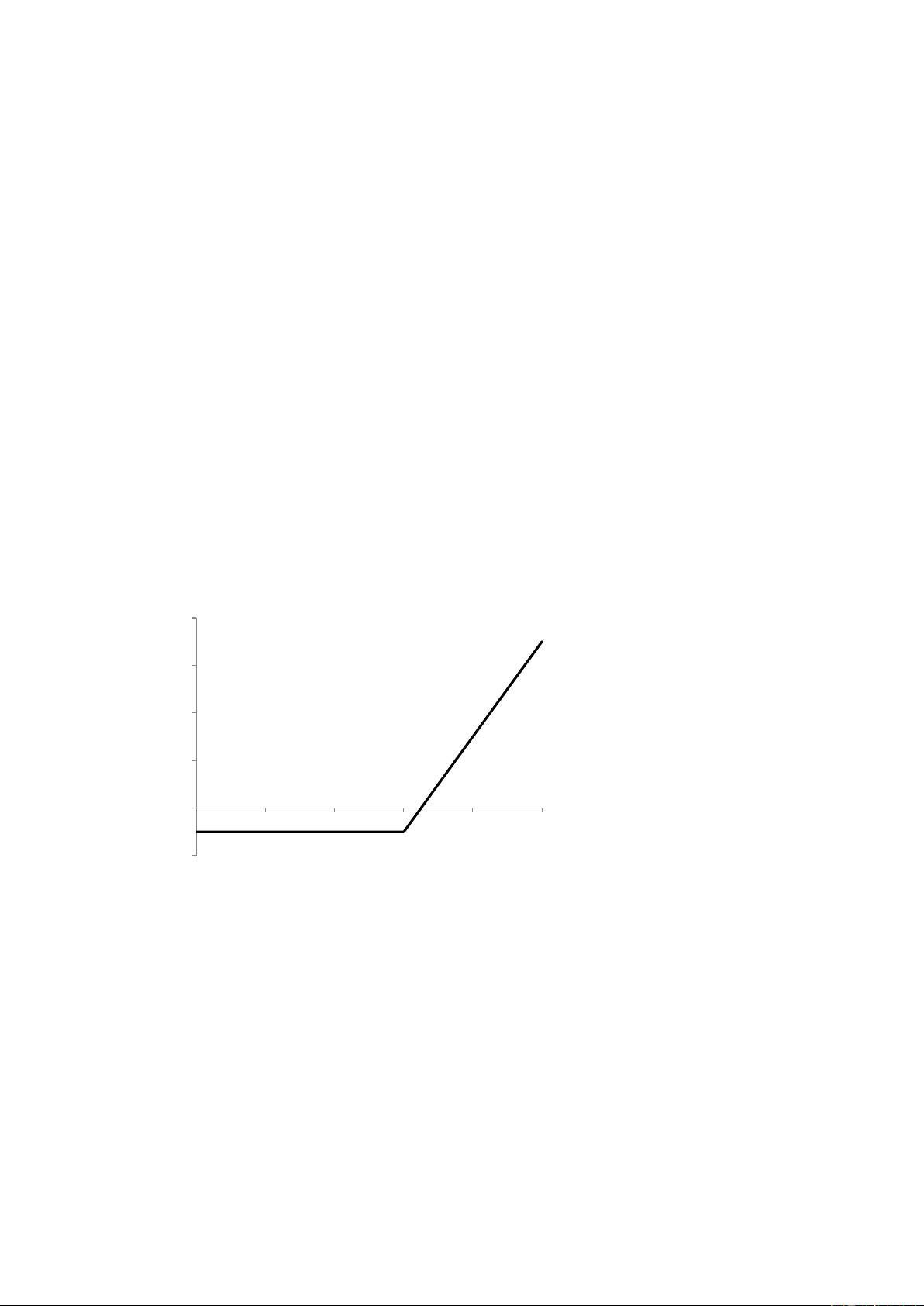

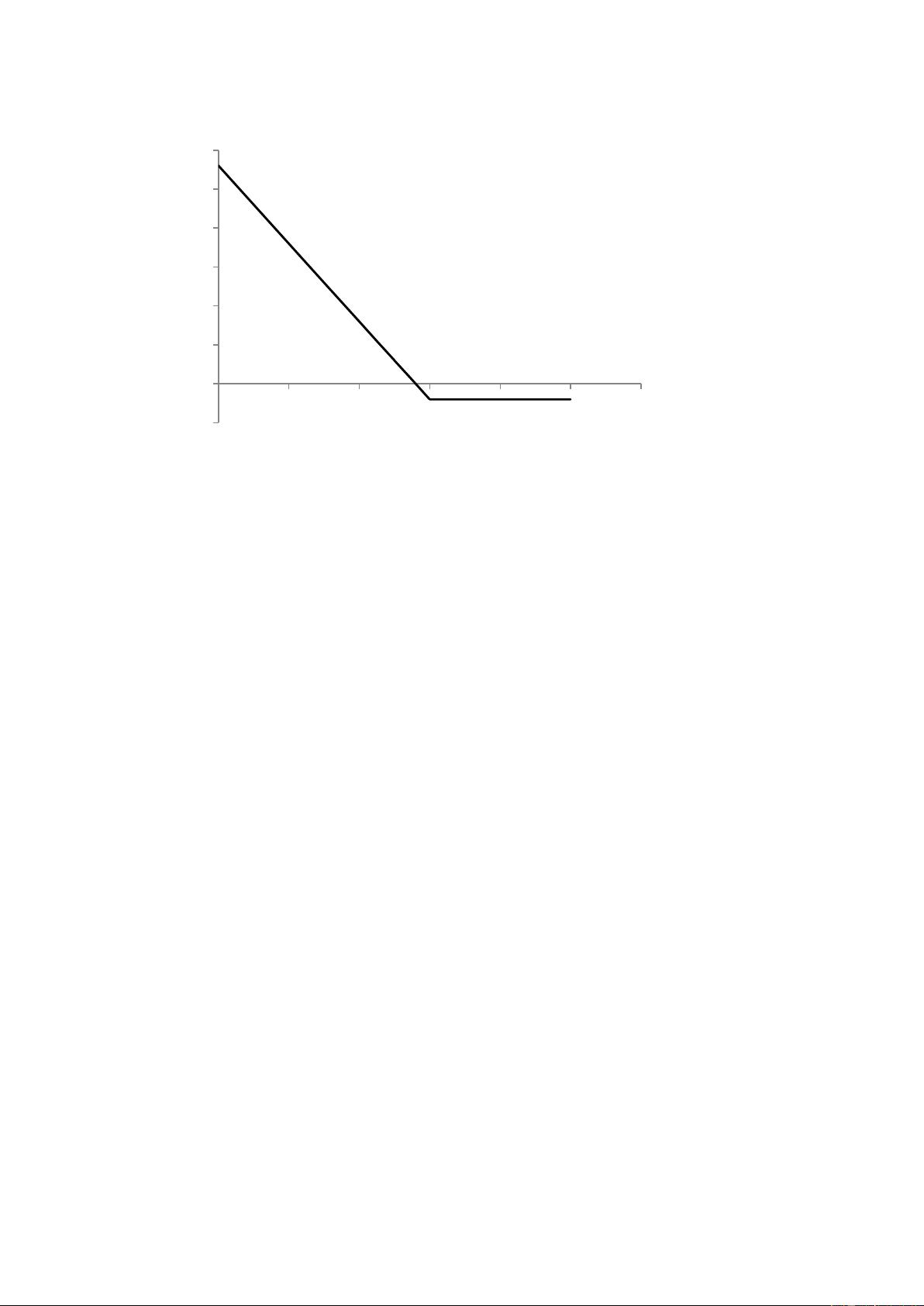

Problem 1.8.

Suppose you own 5,000 shares that are worth $25 each. How can put options be used to

provide you with insurance against a decline in the value of your holding over the next four

months?

You should buy 50 put option contracts (each on 100 shares) with a strike price of $25 and an

expiration date in four months. If at the end of four months the stock price proves to be less

than $25, you can exercise the options and sell the shares for $25 each.

Problem 1.9.

A stock when it is first issued provides funds for a company. Is the same true of an

exchange-traded stock option? Discuss.

An exchange-traded stock option provides no funds for the company. It is a security sold by

one investor to another. The company is not involved. By contrast, a stock when it is first

issued is sold by the company to investors and does provide funds for the company.

Problem 1.10.

Explain why a futures contract can be used for either speculation or hedging.

If an investor has an exposure to the price of an asset, he or she can hedge with futures

contracts. If the investor will gain when the price decreases and lose when the price increases,

a long futures position will hedge the risk. If the investor will lose when the price decreases

and gain when the price increases, a short futures position will hedge the risk. Thus either a

long or a short futures position can be entered into for hedging purposes.

If the investor has no exposure to the price of the underlying asset, entering into a futures

contract is speculation. If the investor takes a long position, he or she gains when the asset’s

price increases and loses when it decreases. If the investor takes a short position, he or she

loses when the asset’s price increases and gains when it decreases.

Problem 1.11.

A cattle farmer expects to have 120,000 pounds of live cattle to sell in three months. The

live-cattle futures contract on the Chicago Mercantile Exchange is for the delivery of 40,000

pounds of cattle. How can the farmer use the contract for hedging? From the farmer’s

viewpoint, what are the pros and cons of hedging?

The farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the

gain on the futures contract will offset the loss on the sale of the cattle. If the price of cattle

rises, the gain on the sale of the cattle will be offset by the loss on the futures contract. Using

futures contracts to hedge has the advantage that it can at no cost reduce risk to almost zero.

Its disadvantage is that the farmer no longer gains from favorable movements in cattle prices.

剩余167页未读,继续阅读

zhouchendd

- 粉丝: 3

- 资源: 6

我的内容管理

收起

我的内容管理

收起

- 我的资源

快来上传第一个资源

我的收益 登录查看自己的收益

我的收益 登录查看自己的收益 我的积分

登录查看自己的积分

我的积分

登录查看自己的积分

我的C币

登录后查看C币余额

我的C币

登录后查看C币余额

我的收藏

我的收藏  我的下载

我的下载  下载帮助

下载帮助

会员权益专享

最新资源

- 27页智慧街道信息化建设综合解决方案.pptx

- 计算机二级Ms-Office选择题汇总.doc

- 单链表的插入和删除实验报告 (2).docx

- 单链表的插入和删除实验报告.pdf

- 物联网智能终端项目设备管理方案.pdf

- 如何打造品牌的模式.doc

- 样式控制与页面布局.pdf

- 武汉理工Java实验报告(二).docx

- 2021线上新品消费趋势报告.pdf

- 第3章 Matlab中的矩阵及其运算.docx

- 基于Web的人力资源管理系统的必要性和可行性.doc

- 基于一阶倒立摆的matlab仿真实验.doc

- 速运公司物流管理模式研究教材

- 大数据与管理.pptx

- 单片机课程设计之步进电机.doc

- 大数据与数据挖掘.pptx

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈

评论0