Stata 7 Reference Manual: Volume 2H-P

需积分: 8 114 浏览量

更新于2024-07-19

收藏 56.22MB PDF 举报

"stata 7 reference manual"

Stata 是一款强大的统计分析软件,广泛用于社会科学、医学研究、经济学和教育学等领域。Stata 7 Reference Manual 是该软件的官方指南,提供了关于Stata 7版本的所有功能和操作的详细说明。这本书由StataPress出版,分为四个卷,涵盖了从基础统计分析到高级方法的各种主题。

本手册包含的内容可能包括但不限于以下部分:

1. **数据管理**:Stata 7提供了强大的数据管理工具,包括数据导入、导出、变量创建、排序、合并和分组等。用户可以学习如何有效地组织和预处理数据。

2. **统计分析**:手册详细介绍了各种统计模型,如描述性统计、t检验、ANOVA、回归分析(线性和非线性)、逻辑回归、生存分析、面板数据模型等。

3. **图形制作**:Stata 7支持创建各种高质量的统计图形,如散点图、箱线图、直方图、生存曲线等,用户可以学习如何定制和美化图形。

4. **编程与宏**:Stata具有内置的命令语言,用户可以通过编写do文件进行批处理操作。手册会解释如何编写和使用do文件,以及如何创建自定义命令和宏。

5. **随机过程与仿真**:对于需要模拟数据或进行复杂计算的研究者,手册将提供有关随机数生成和模拟技术的信息。

6. **估计结果的解释与检验**:手册将指导用户如何理解和解释统计模型的估计结果,包括系数的显著性测试、残差分析和诊断测试。

7. **高级统计方法**:Stata 7支持多种高级统计技术,如GARCH模型、非参数方法、多层模型、有限混合模型等,手册将详细介绍这些方法的应用和实现。

8. **更新与改进**:手册中会提到Stata 7相对于之前版本的改进和新增功能,这可能包括更快的计算速度、更多的统计命令以及对新数据格式的支持。

值得注意的是,虽然手册声明所有权利保留,并且不提供任何明示或暗示的保修,但StataCorp可能会在任何时候对产品和程序进行改进和更改,因此实际使用时应参考最新的文档或软件版本。

Stata 7 Reference Manual 是Stata用户必备的参考资料,无论是初学者还是经验丰富的用户,都可以从中获得深入的理解和实践指导,以充分利用Stata的强大功能。

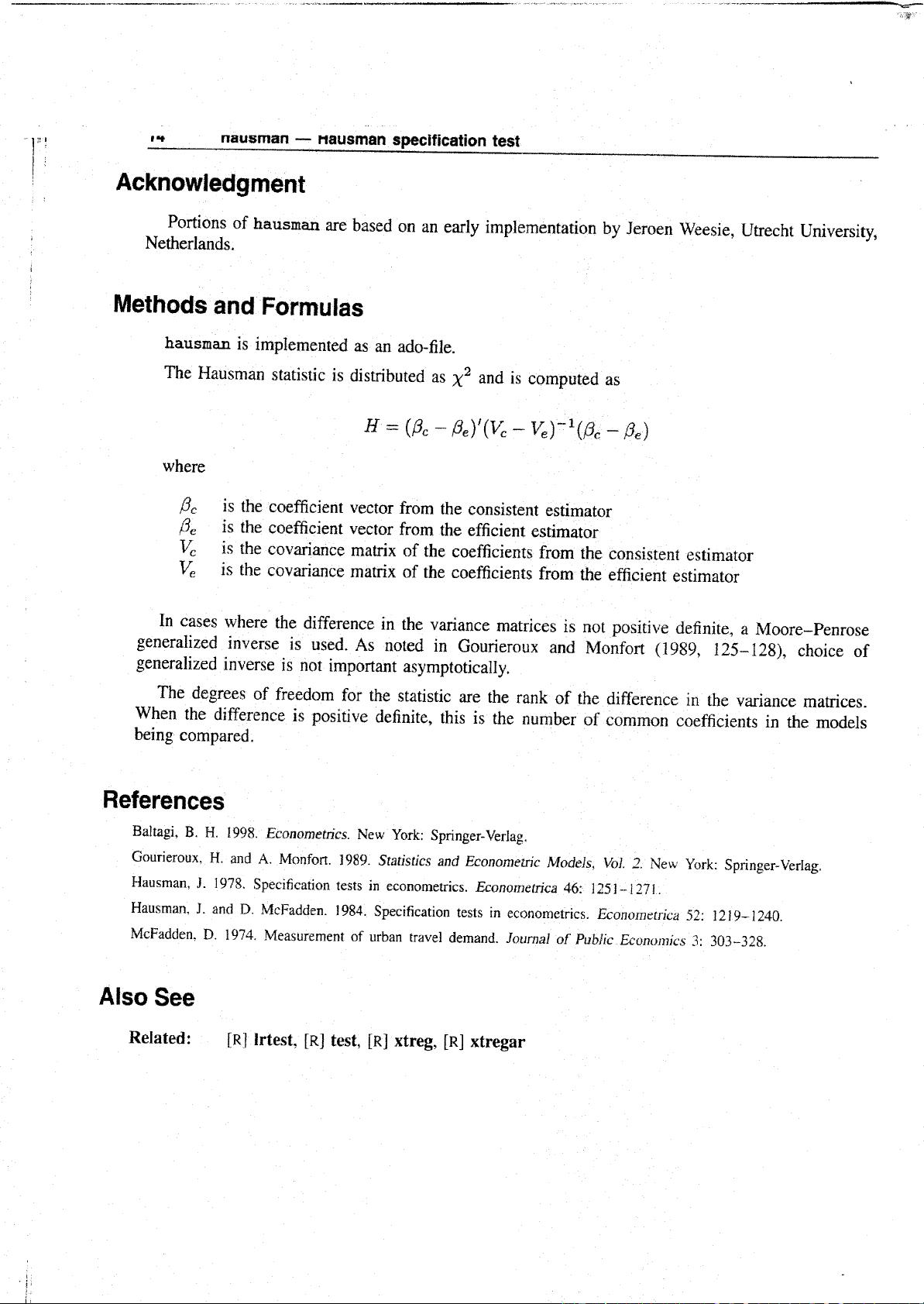

1:,, ,,_ nausman -- Nausman specification test

!_ Acknowledgment

Portions of hausman are based on an early implementation by Jeroen Weesie, Utrecht University,

Netherlands.

' Methods and Formulas

hausman is implemented as an ado-file.

The Hausman statistic is distributed as X 2 and is computed as

//- (/3c-/_e)'(_ - _)-1(/_c 9e)

where

tic is the coefficient vector from the consistent estimator

3e is the coefficient vector from the efficient estimator

V_ is the covariance matrix of the coefficients from the consistent estimator

V_ is the covariance matrix of the coefficients from the efficient estimator

In cases where the difference in the variance matrices is not positive definite, a Moore-Penrose

generalized inverse is used. As noted in Gourieroux and Monfort (1989, 125-128), choice of

generalized inverse is not important asymptotically.

The degrees of freedom for the statistic are the rank of the difference in the variance matrices.

When the difference is positive definite, this is the number of common coefficients in the models

being compared.

References

Baltagi, B. H. 1998.Econometrics. New York:Springer-Verlag.

Gourieroux, H. and A. Monfort. 1989. Statistics and Econometric Modets, Vol. 2. New York: Springer-Verlag.

Hausman, J. 1978. Specificationtests in econometrics. Econometrica46: 1251-1271.

Hausman, J. and D. McFadden. 1984. Specificationtests in eco_ometncs. Econometrica52. 12t9-1240.

McFadden, D. 1974. Measurement of urban travel demand. Journal of Public Economics 3: 303-328.

Also See

Related: [R| lrtest, [R] test, [R] xtreg, [R] xtregar

i:

剩余591页未读,继续阅读

136 浏览量

251 浏览量

290 浏览量

136 浏览量

173 浏览量

110 浏览量

3030 浏览量

2502 浏览量

Jasonzhang1011

- 粉丝: 0

- 资源: 1

我的内容管理

展开

我的内容管理

展开