"全球宏观策略:德国央行温和转向持续"

下载需积分: 0 | PDF格式 | 1.8MB |

更新于2024-04-15

| 72 浏览量 | 举报

JP Morgan Global Macro Strategy released a report titled "Core Currency Views: Germany's Bundesbank Mild Pivot Continues to Unfold" which discusses the gradual shift in stance by the German central bank. The report delves into the implications of this shift on global currency markets and offers insights on potential trading strategies.

According to the report, the Bundesbank's subtle change in direction reflects a broader trend of central banks around the world reassessing their monetary policies in response to changing economic conditions. While the Bundesbank is known for its conservative approach, the report suggests that it is now more open to making adjustments in order to support the German economy amid global uncertainties.

The report highlights the importance of monitoring the Bundesbank's policy announcements and speeches for clues on future monetary policy decisions. It also emphasizes the need for market participants to stay nimble and adapt their trading strategies to changing central bank dynamics.

Overall, the report provides a comprehensive analysis of the evolving stance of the German central bank and its potential impact on global currency markets. It serves as a valuable resource for investors looking to navigate the complexities of the foreign exchange market in light of changing central bank policies.

For more information and to access the full report, interested parties can visit the JP Morgan Global Macro Strategy website at www.jpmm.com/Research/GlobalFXStrategyGlobal FX Strategy.

8

Global FX Strategy

18 March 2019

Daniel P Hui

(1-212) 834-5997

daniel.hui@jpmorgan.com

Patrick R Locke

(1-212) 834-4254

patrick.r.locke@jpmchase.com

JPM USD Index

Table 1: JP Morgan Forecasts

Source: J.P. Morgan

Near-term USD strength against mounting

chronic vulnerabilities

This month, we upgrade our dollar forecast horizon

against G10 FX on the back of global central banks

following the Fed's dovish footsteps, coupled with a

still-muddling global growth backdrop and some

idiosyncratic risks coming to the fore. We also roll out

our fresh forecasts for 1Q’20. The most notable revision

is a downgrade to EUR, now expected to reach 1.16 by

year-end (prev. 1.20) and then to 1.17 in early 2020. We

also revise CAD weaker by year-end to 1.33 (prev. 1.28)

and 1.31 in 2020. In the past month, we've also trimmed

our AUD forecast to 0.66 by year-end from 0.68, while

NZD is now 0.65 (from 0.63). Rounding out G10, GBP

is revised incrementally stronger vs USD, NOK and

SEK are downgraded alongside EUR, and JPY is

unchanged with its new 1Q'20 forecast flat from year-

end 109. On the other hand, our 2019 EM forecasts are

unchanged in Latam and Asia (CNY flat in 1Q’20 at

6.65), but with parts of EMEA dragged down by the

revision to EUR. Taken altogether, our USD forecasts

are upgraded 1% on average and now project fairly flat

into Dec ‘19.

The dollar has remained stubbornly resilient as

dovish shifts elsewhere have followed the Fed’s

earlier move. In the wake of the Fed’s dovish U-turn in

late January, we had argued that the dollar would still

struggle to broadly weaken, particularly against other

G10 currencies which were lower yielding and were

even more vulnerable to their own dovish monetary

policy shifts. In the past month, this has played out with

significant dovish policy shifts particularly in AUD,

CAD, and EUR driving these currencies materially

lower versus the dollar (see More Problems, More

Money, More Dollar Strength, 8 March). Meanwhile on

growth momentum models, the USD is now as much as

4% cheap, primarily due to the fact that markets seem to

be looking through the recent sharp slowdown in the

global cycle on hopes that stimulus and trade war

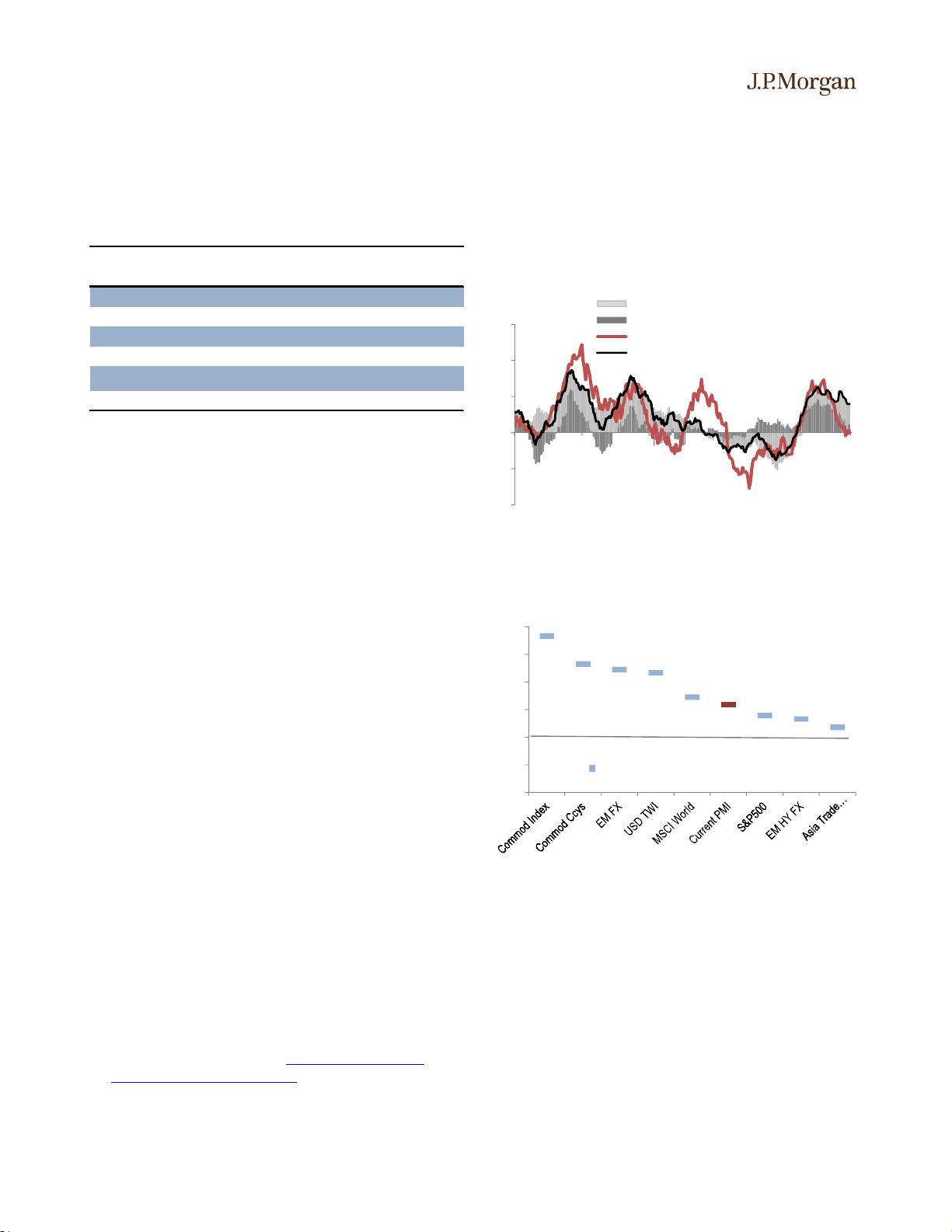

Exhibit 1: USD remains 4.0% cheap to growth momentum models

underscoring the global growth rebound hurdle for more broad-

based dollar weakness.

USD %6m = 0.054+ 4.31 * (US-Global FRI) - 6.45 * (Global FRI), R=59%

Source: JPMorgan

Exhibit 2: Current dollar weakness implies a global growth

environment that is a point higher on the global mfg PMI scale

Implied PMI levels based on univariate regression of 12m change in asset

on global manufacturing PMIs (5-year lookback)

Source: JPMorgan

de-escalation will drive a bounce in global activity

(Exhibit 1). Consequently the dollar has not received

the anti-cyclical bid that would otherwise be consistent

with the recent acute slowdown in the global

manufacturing cycle. This additional dollar discount

versus slowing growth momentum combines with

USD's high-yielding status and limited scope for further

Fed depricing, all of which add up to significant

observed dollar resilience amid a dovish Fed.

Thus, the hurdle for broader dollar weakness to

manifest is a material rebound in global growth in

the rest of the world. In addition to the reliance on

greater confidence in the growth outlook by central

banks to halt or reverse the slide in other G10 monetary

Jun 19 Sep 19 Dec 19 Mar 20

USD GDP (% saar) 2.3 1.8 1.8 1.8

Global GDP growth 3.0 3.0 2.6 2.9

USD policy rate (%) 2.50 2.50 2.50 2.50

Global ex-USD policy rate 2.78 2.75 2.71 2.78

DXY 97.6 96.1 94.5 93.8

JPM USD Index 122.0 121.7 120.9 na

-10

-5

0

5

10

15

Mar-14 Mar-15 Mar-16 Mar-17 Mar-18

Mar-19

Contribtuion of lower Global FRI

Contribution of widening US-Global FRI spd

USD Index, %6m

USD Index FRI Model (Global & US-Global), 5y

49.0

49.5

50.0

50.5

51.0

51.5

52.0

Implied PMI

剩余42页未读,继续阅读

相关推荐

2301_76429513

- 粉丝: 15

我的内容管理

展开

我的内容管理

展开

最新资源

- 最新IP地址互查工具V0.94版发布

- 基于JSP+Servlet+JavaBean+MySQL构建投票评估系统

- 64位TortoiseSVN中文版安装包下载指南

- JAVA实现的ID3与C4.5算法公共代码包

- 数字钟设计与仿真:电子技术课程项目解析

- 善领DSA升级助手V1.0发布:简化电子狗升级流程

- MARS火星ERP:面向制造业的综合管理系统

- Android音乐播放器源码解析与开发指南

- SystemC 2.0:电子系统设计的高效工具

- C#编程实现经典游戏—撞砖头

- H3C MIB库文件合并介绍 - 兼容与公有MIBs

- PPT演示助手 PPtShow v1.0 功能介绍与使用指南

- C++编译原理课程设计:词法分析程序实例解析

- 探索Github博客网站:米尔的Ruby与HTML实践

- 深入浅出:基于C++实现蚁群算法全过程

- ADSL密码备份工具:轻松备份与恢复