第一章 引言 自回归时间序列误差分位数的默示有效估计及预测区间

为了说清楚这一点, 我们结合文献[17]考虑了非正态误差的AR(2), 以及本文关于

应用的第四章里的油价实例, 这两者都揭示了正态PI的覆盖频率已经相当偏离事先既

定的置信水平, 见表格3.1, 3.2和4.3. 从表格中,我们可以看到正态PI没有默示PI (本

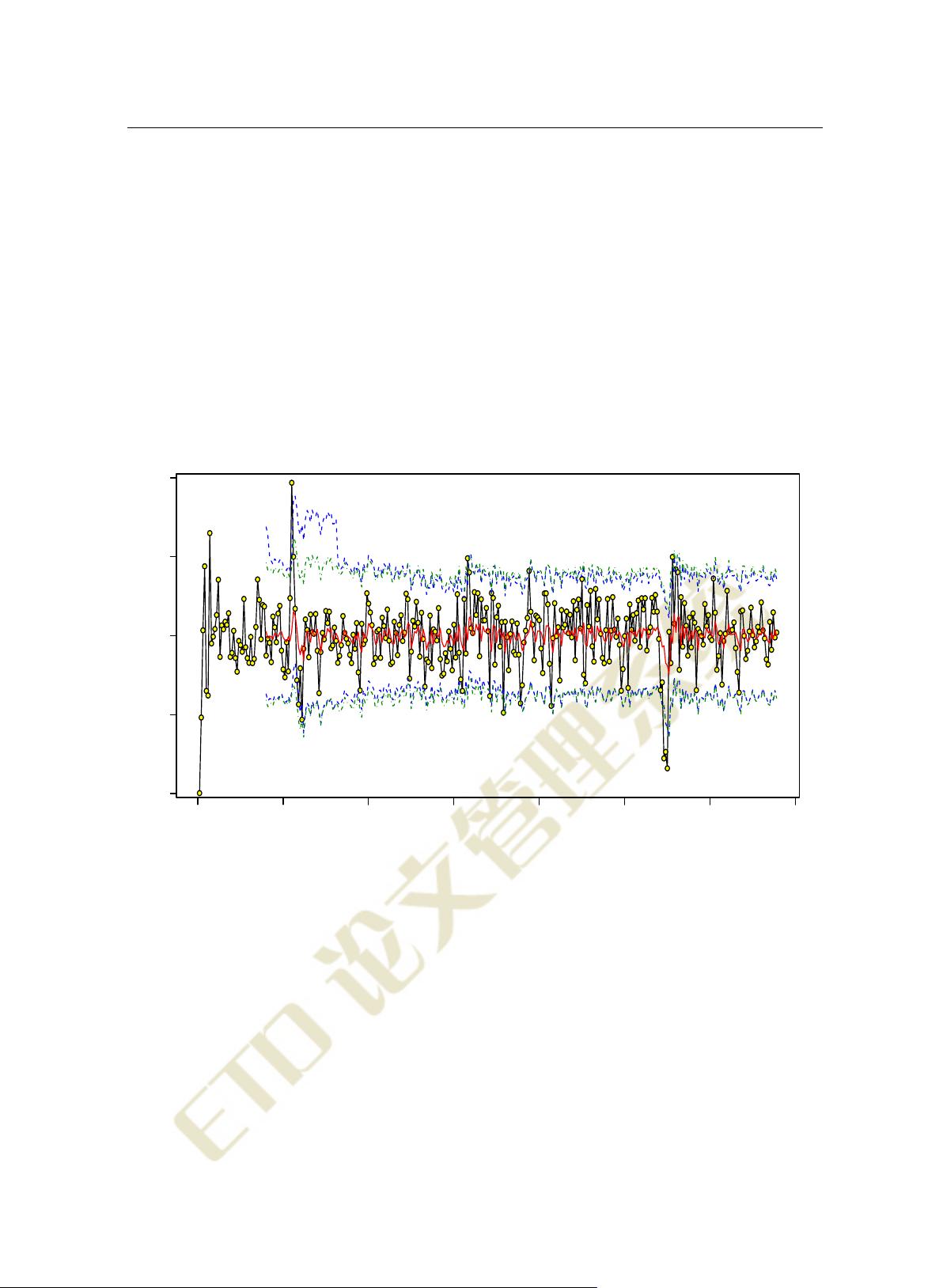

文提出的,下文讨论)来得准确. 在图1.1中,我们给出超过300个的滚动预测来比较正

态PI与默示PI, 发现默示PI更适应动态数据. 默示PI背后的思想接近于文献[29]里的光

滑自助法(Smooth Bootstrap), 但是在本质上拓展了残差替代误差的观点.

0 50 100 150 200 250 300 350

−0.4 −0.2 0.0 0.2 0.4

Time

oil price

图 1.1: 原油价格的AR(1)模型拟合与滚动预测: 实际观测值(圆圈), 预测值(中间实线),

95% 默示PI (虚线), 95% 正态PI (虚线和点).

假设q

α

1

和q

α

2

分别是F (z)的α

1

和α

2

分位数, 0 < α

1

< α

2

< 1, 1 − α = α

2

− α

1

. 因

为P

X

n+1

∈

˜

X

n+1

+ q

α

1

,

˜

X

n+1

+ q

α

2

= P (Z

n+1

∈ [q

α

1

, q

α

2

]) = α

2

−α

1

, 其中

˜

X

n+1

=

ϕ

1

X

n

+ ··· + ϕ

p

X

n−p+1

, 如果当误差分布已知, 我们就可以得到X

n+1

的正确的(1 −α)

PI: [

˜

X

n+1

+ q

α

1

,

˜

X

n+1

+ q

α

2

]. 而现实中的F (z)未知, 这个正确的PI实际上是得不到的.

所以我们称之为不可行PI(Infeasible PI). 在本文的第三章, 我们在各种情况中模拟了

2

剩余25页未读,继续阅读