移动开发现状与经济:平台之争与开发者优先级

需积分: 10 177 浏览量

更新于2024-07-23

收藏 4.01MB PDF 举报

"VisionMobile-Developer Economics Q1 2014"

这篇报告深入探讨了2014年第一季度全球移动开发领域的关键趋势、平台竞争、开发者优先级与平台忠诚度,以及盈利策略。以下是报告的主要内容:

1. 开发者经济:一个680亿美元的应用经济体

在2014年的第一季,移动应用经济已经达到了680亿美元的规模,揭示了移动开发的惊人潜力。这包括应用销售、广告收入、订阅服务和其他相关的数字商品和服务。开发者在这个市场中的角色变得越来越重要,他们的创新和努力推动了这个行业的快速增长。

2. 平台赢家与输家

报告分析了不同移动平台(如iOS、Android、Windows Phone等)的表现,揭示了哪些平台正在赢得市场份额,而哪些可能在失去开发者和用户的青睐。例如,Android凭借其庞大的用户基础和开放性吸引了大量开发者,而iOS则以其高用户价值和付费意愿保持着强大的吸引力。

3. 开发者的优先级与平台忠诚度的对决

开发者在选择平台时,不仅考虑市场规模,还会权衡开发工具的质量、社区支持、盈利潜力等因素。此章节讨论了开发者如何在多个平台上平衡投入,以及哪些平台能够保持开发者对其的忠诚度。

4. 钱在哪里?

报告探讨了开发者如何赚钱,包括应用内购买、广告收入、付费下载等模式。它强调了理解用户行为、定位目标市场和优化用户体验对于提高盈利能力至关重要。

5. 开发工具:更好、更快、更多

随着开发工具的不断进化,开发者能够更高效地创建和优化应用。报告列举了当时市场上的一些优秀工具,这些工具帮助开发者提高了生产力,缩短了产品上市时间,并提升了应用的质量。

报告还提到了VisionMobile举办的“移动商业模式的机制”研讨会,旨在为执行官、经理、企业家和投资者提供关于数字创新策略的洞见。

VisionMobile是一家专注于移动行业分析的公司,致力于为决策者提供关于市场趋势、开发者行为和商业策略的深入见解。通过这份报告,读者可以深入了解2014年移动开发行业的现状和未来方向,对于理解当前移动开发生态系统的发展历程具有重要的参考价值。

© VisionMobile 2014 | www.DeveloperEconomics.com/go

9

CHAPTER ONE

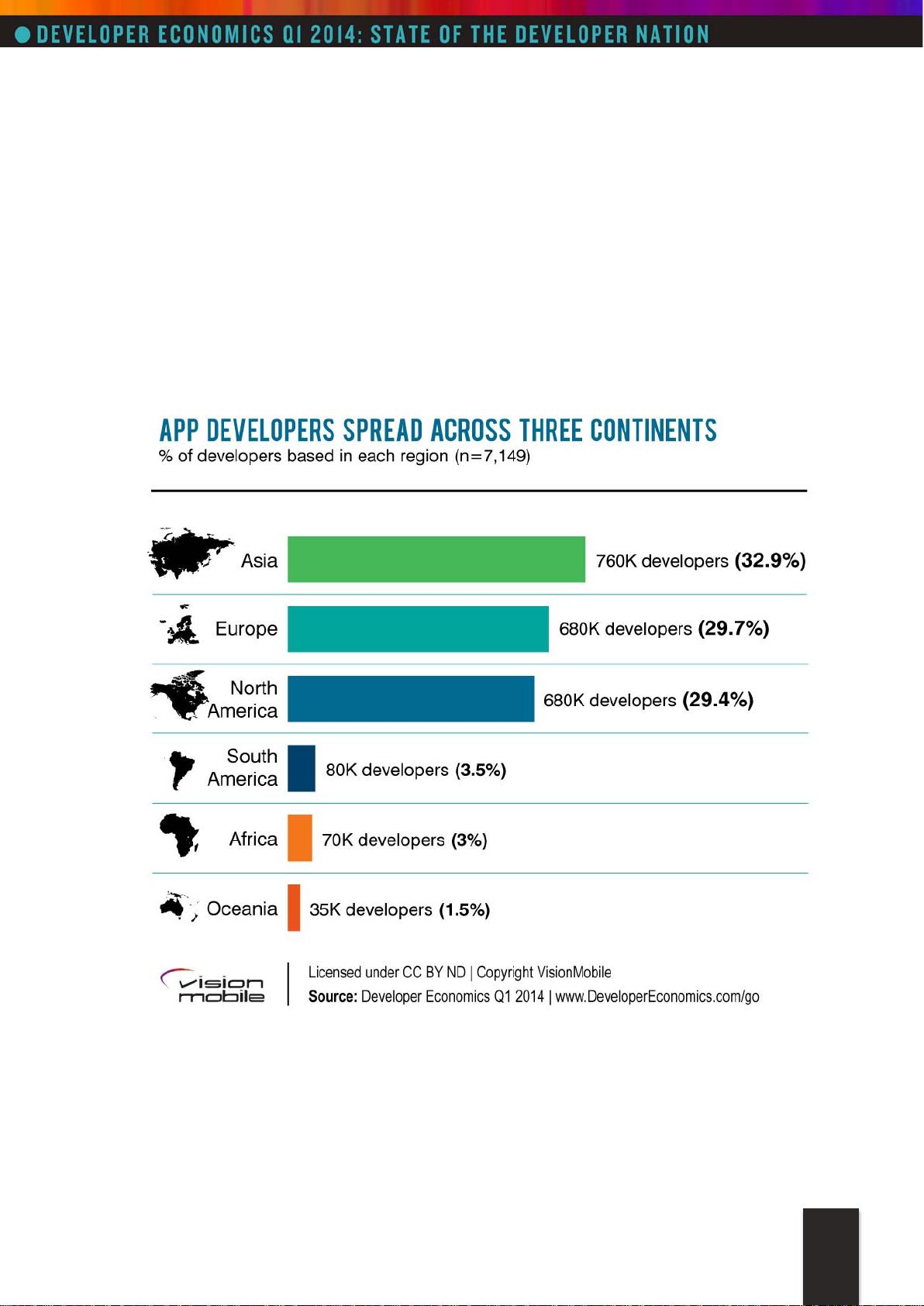

1. A $68 billion app economy

The global app economy was worth $68 billion in 2013 and is projected to

grow to $143 billion in 2016. Out of a total global mobile developer

population of 2.3 million individuals in 2013, Asia has the most app

developer citizens at 760,000 individuals.

For more forecasts on developer population, platforms, revenues and

revenue models see our App Economy Forecasts 2013-2015 report.

1.1. Methodology: reaching 7,000 developers

Developer Economics 6th edition is the largest ever research on app

developers and trends in app development. This report is based on a large-

scale online developer survey and one-to-one interviews with mobile app

developers. The online survey was designed, produced and carried out by

剩余54页未读,继续阅读

2014-02-28 上传

2011-11-16 上传

2010-10-24 上传

点击了解资源详情

2024-12-30 上传

2024-12-30 上传

2024-12-30 上传