21 December 2018 12

21 December 2018

Hong Kong

EQUITIES

3355 HK

Not rated

Stock price as of 19/12/2018

HK$

1.45

GICS sector

Semiconductors

Market cap

US$m

284

Avg Value Traded (3m)

US$m

1

12m high/low

HK$

1.41/0.69

PER FY17

x

33.2

P/BV FY17

x

2.0

Historical financials

YE Dec (HK$ m)

2015A

2016A

2017A

Revenue

741

796

1013

% growth

-7%

7%

27%

EBITDA

91

94

125

% growth

-14%

4%

32%

EPS

0.02

0.02

0.04

% growth

-30%

-5%

76%

EBIT Margin

3.3%

3.0%

4.5%

Source: Company data, FactSet, December 2018

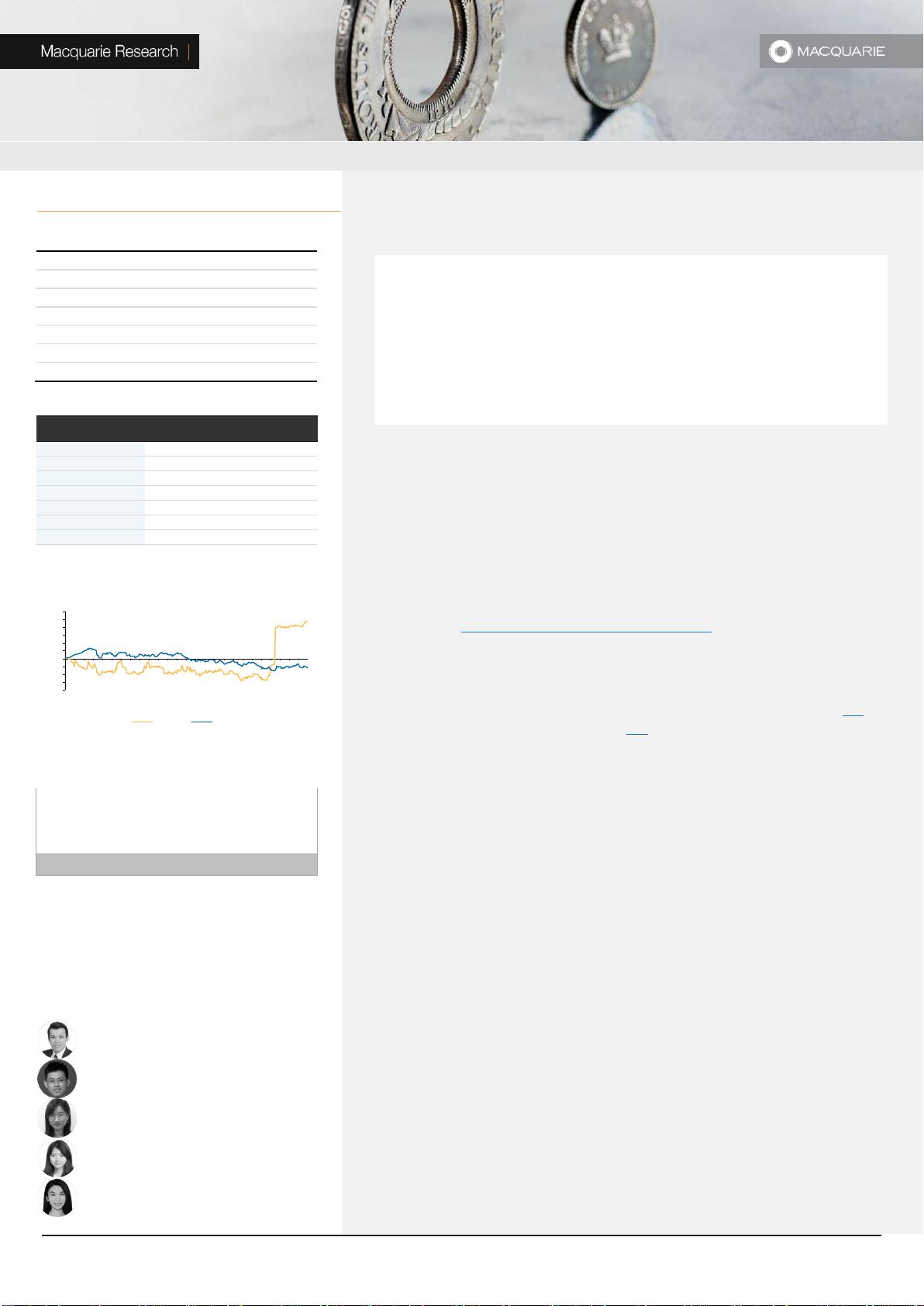

ASMC’s stock performance vs. HSI

Source: Bloomberg, December 2018

Share Price Driver

Thematic

Growth

Value

Event

Source: Macquarie Research, December 2018

Analysts

Macquarie Capital Limited

Allen Chang +852 3922 1136

allen.chang@macquarie.com

Jin Guo +86 21 2412 9054

jin.guo@macquarie.com

Fiona Liu +852 3922 1368

fiona.liu@macquarie.com

Verena Jeng +852 3922 3766

verena.jeng@macquarie.com

Heidi Leung +852 3922 3783

heidi.leung@macquarie.com

MacVisit: ASMC

Specialty foundry being taken private

Key points

ASMC is a foundry that manufactures 5'', 6'', 8'' wafers for analog and power

discretes; End applications: automobile, consumer electronics, etc.

ASMC’s 6’’ and 8’’ capacity is tight due to strong demand for its 6’’/8’’

products including MOSFET, IGBT, Power IC, TVS, etc.

Per mgmt, ASMC faces an urgent need to expand capacity and upgrade

technology and privatization by Huada will allow ASMC to do so.

Event

We visited ASMC (先进半导体) and discussed with mgmt its business outlook

and capex plans. A key point stressed by mgmt was that ASMC enjoys a

solid demand outlook but lacks the production capacity to fully capture

the opportunities. Utilization rate reached 112% for its 6’’ fab and 94% for 8’’

fab in 3Q18. Mgmt expressed the urgent need for capital to expand capacity

and upgrade technology to stay competitive. More recently, ASMC announced

that it is being taken private by Huada (a SOE) at HK$1.5/share, or a 67%

premium over its stock price prior to the announcement (see more details in

our report: Huada acquiring ASMC at HK$1.5/share). ASMC expects to gain

access to the much needed capital to address the capacity challenge.

The ASMC deal supports our view of China’s continuous efforts to

strengthen the ecosystem and show strong support for the

semiconductor industry. Read-across to other China foundries: SMIC (link,

Nov 8) and our top pick, Hua Hong (link, Nov 9).

Key discoveries

Craving for capital to expand capacity: ASMC has been running at ~100%

capacity utilization and its 6’’ and 8’’ products including MOSFET, IGBT, TVS,

etc. are in strong demand. ASMC has been looking for funding to expand

capacity to capture the demand. After the acquisition, ASMC expects to gain

access to the much needed capital to expand capacity. ASMC primarily

focuses on 6’’ and 8’’ products, each accounting for ~47% of total sales.

Positive outlook in 4Q18; momentum to continue on strong orders: Mgmt

expects growth momentum to continue in 4Q18 given strong orders intake

from both domestic and overseas customers. In terms of capacity expansion,

8’’ fab capacity expanded by 8% YoY in 3Q18 to 28k wpm. 6’’ fab capacity has

been stable at 24k wpm (8’’ equivalent) in 3Q18. Mgmt will continue to improve

productivity, efficiency and product mix for 6’’ fab to drive revenue growth

despite utilization rate for 6’’ fab is at 112% in 3Q18.

IGBT: ASP increase and close cooperation with BYD; ASMC is in close

cooperation with BYD on IGBT and expects BYD revenue contribution to

double to 10% in 2019E. ASMC’s IGBT products range from 1200V to 6500V

and enjoys ASP increase due to tight supply, according to management.

ASMC also saw a 20~30% price hike for MOSFET this year.

Financials and industry downside risks

The stock trades at 33x 2017 PE and 2x 2017 PB with an average of ROE of

4% during 2015-17. Risks include US-China trade war escalation, China’s

macro slowdown and volatile foreign exchange fluctuations.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Dec-17

Jan-18

Jan-18

Jan-18

Feb-18

Feb-18

Mar-18

Mar-18

Apr-18

Apr-18

May-18

May-18

Jun-18

Jun-18

Jul-18

Jul-18

Aug-18

Aug-18

Aug-18

Sep-18

Sep-18

Oct-18

Oct-18

Nov-18

Nov-18

Dec-18

ASMC HSI

ASMC: +58% YTD

HSI: -12% YTD

剩余68页未读,继续阅读

制了个了个杖

- 粉丝: 25

- 资源: 499

我的内容管理

展开

我的内容管理

展开

最新资源

- 多模态联合稀疏表示在视频目标跟踪中的应用

- Kubernetes资源管控与Gardener开源软件实践解析

- MPI集群监控与负载平衡策略

- 自动化PHP安全漏洞检测:静态代码分析与数据流方法

- 青苔数据CEO程永:技术生态与阿里云开放创新

- 制造业转型: HyperX引领企业上云策略

- 赵维五分享:航空工业电子采购上云实战与运维策略

- 单片机控制的LED点阵显示屏设计及其实现

- 驻云科技李俊涛:AI驱动的云上服务新趋势与挑战

- 6LoWPAN物联网边界路由器:设计与实现

- 猩便利工程师仲小玉:Terraform云资源管理最佳实践与团队协作

- 类差分度改进的互信息特征选择提升文本分类性能

- VERITAS与阿里云合作的混合云转型与数据保护方案

- 云制造中的生产线仿真模型设计与虚拟化研究

- 汪洋在PostgresChina2018分享:高可用 PostgreSQL 工具与架构设计

- 2018 PostgresChina大会:阿里云时空引擎Ganos在PostgreSQL中的创新应用与多模型存储

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈